Table of Contents

Frequently Asked Questions

1. Can a free zone company in Dubai apply for a business loan?

Yes. Free zone companies, including those registered at Meydan Free Zone, can apply for business loans through UAE banks and financial institutions. A valid trade license, corporate bank account, and at least one year of operating history are typically required.

2. What is the minimum turnover required to get a business loan in Dubai?

Most UAE banks require a minimum annual turnover of AED 1 million, though this varies by institution and loan type. Some government-backed SME programmes have lower thresholds for qualifying businesses.

3. How long does it take to get a business loan approved in Dubai?

Approval timelines vary by lender. Many banks now offer online applications with decisions in 5 to 10 working days. Complex applications or those requiring additional documentation can take longer.

4. What is the difference between a standard bank loan and Islamic finance in the UAE?

A standard bank loan charges interest on the borrowed amount. Islamic finance is Sharia-compliant and operates on profit-and-loss sharing rather than interest. The end result — access to capital — is the same, but the contractual structure differs significantly.

5. What happens if my business loan application is rejected?

If your application is rejected, consider an SBA-backed loan (UAE government-supported), improve your credit score, reduce existing debt, or seek support from a Meydan Free Zone banking advisor who can guide you towards lenders suited to your profile.

6. Does Meydan Free Zone help with business loan applications?

Meydan Free Zone provides banking support through Meydan Plus, including introductions to 26+ banking partners, document preparation guidance, and account opening assistance — all of which strengthen a business loan application.

Topic Summary

1. Assess Your Business Needs and Eligibility

Before initiating the loan application, clearly define the purpose and amount of funding required. Evaluate your business’s financial health, creditworthiness, and eligibility criteria set by lenders. In Dubai, business loans typically demand a solid business plan, positive cash flow, and relevant documentation proving business legitimacy.

2. Prepare Required Documentation

Gather all necessary paperwork, including your trade licence, Memorandum of Association (MOA), financial statements, bank statements, and personal identification documents. Additional requirements may include cash flow projections, invoices, and a detailed business plan outlining how the funds will be utilised.

3. Choose the Appropriate Lender

Research and compare various banking institutions and financial service providers in Dubai. Consider the loan types they offer, interest rates, repayment terms, and eligibility conditions. Dubai offers business loans through conventional banks, Islamic finance institutions, and specialised lending platforms, each with distinct terms.

4. Submit the Application

Complete the lender's application form accurately, attaching all required documents. Many institutions now offer online loan applications, enabling quicker processing. Ensure you disclose all relevant information to prevent delays or rejections during the assessment phase.

5. Loan Processing and Disbursement

After submission, the lender will evaluate your application, conduct credit assessments, and may request additional information. Upon approval, you will receive a loan offer outlining terms and conditions. Review the agreement meticulously before signing. Once finalised, funds will be disbursed as per the agreed schedule, allowing you to utilise the capital for your business objectives.

How to Apply for a Business Loan in Dubai: A Step-by-Step Guide

A business loan can prove useful in instances where you need a financial boost to jump-start your newly registered business, or require financial collateral to open up another branch and generate higher sales. Raising capital and gaining investment can be a daunting task for some newly established businesseshowever, to have a smooth flow in the long-term, or your day-to-day operations, securing loan funding is a must.

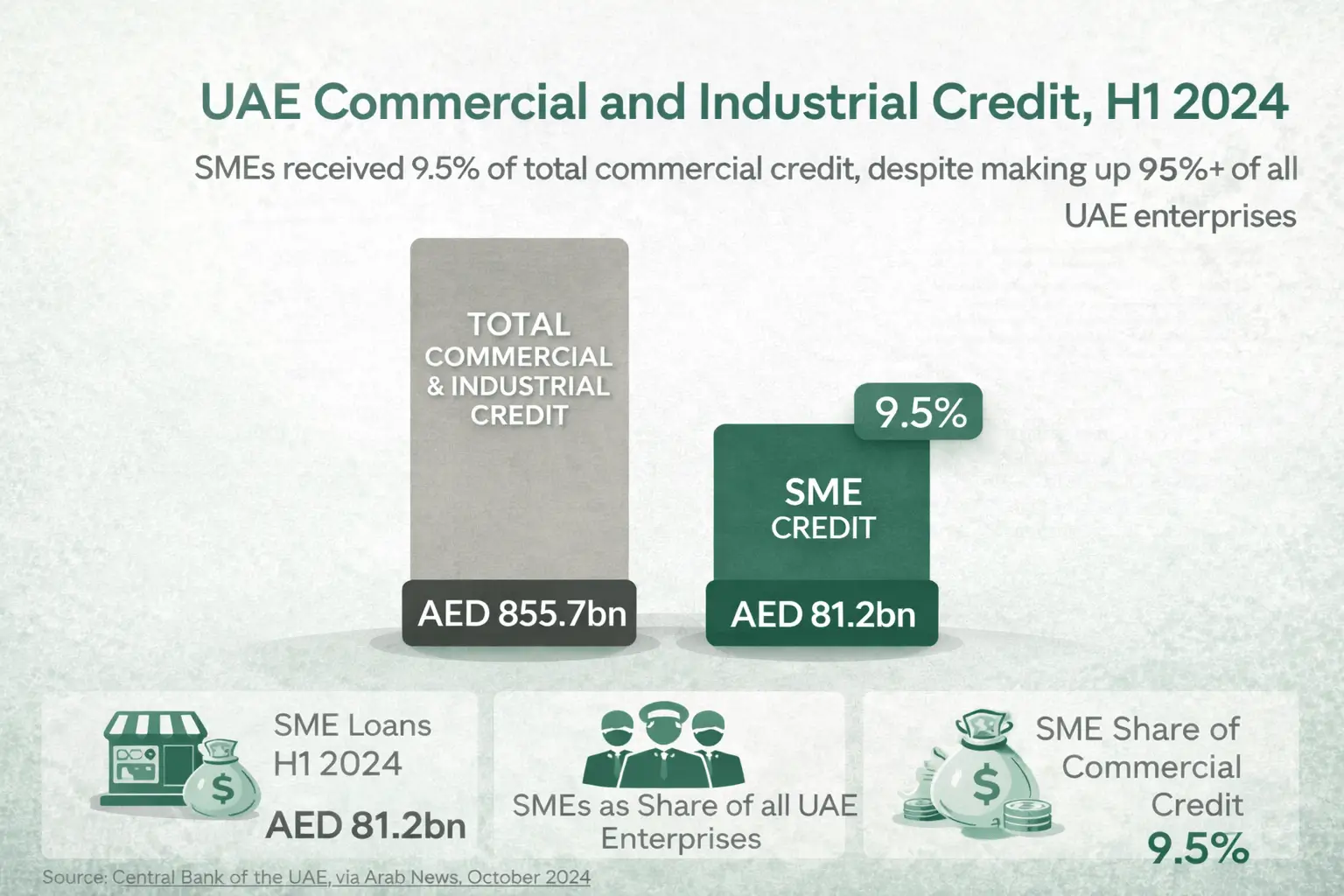

Before you apply, it helps to understand the landscape you are entering: UAE banks are extending hundreds of billions in commercial credit, and the gap between what SMEs represent economically and what they currently receive from lenders is exactly why preparation matters.

Source: Central Bank of the UAE, via Arab News, October 2024

With AED 93.4 billion being provided to enterprises by Emirate banks, Dubai is considered an attractive location for SMEs to plan for the long term and secure their cash flow. To empower your business financially, equip yourself with knowledge about this process first. At Meydan Free Zone, the process of documentation and loan preparation can be managed by our panel of consultants.

[blockCTATradeLicense]

Features of Business Loans in UAE

A business loan is borrowed capital granted specifically for entrepreneurial purposes. The UAE conforms to its own regulatory environment, and certain conditions apply to how Emirate banks carry out transactions. Before we delve into the specifics of eligibility and benefits, its important to be aware of the important characteristics of a business loan.

The new entry permits and tourist visa changes that will come into effect October 3 2022:

- Loan Amount Provided

Depending on the type of loan you decide to apply for, whether it be an Islamic loan or a small business loan, the amount you receive will vary from AED 50,000 to AED 7 million. The loan applicants liquidity history and assets will be taken into account when arriving at a consensus. - Interest Rates

On average, Dubais interest rates range from approximately 15% to 26% with favourable conditions. The fluctuation of the interest rate will depend on the applicants credit history, income, number of loans and other financial collateral. - Bank Account

The business must have a functioning bank account in the UAE assigned to them in order to apply. The bank will analyse all transactions and relationships with the lender to decide whether the loan should be granted or not. - Payment Period

In Dubai, the repayment period for a business loan ranges from 2 to 5 years, depending on your funds and the amount taken.

Other than this, you will also encounter a minimal amount of documentation and paperwork to go through, whilst having a consultant to guide you through any doubts during the process. At Meydan Free Zone, the process of hefty documentation and applying for a business loan can be managed by our panel of talented consultants.

Types of Business Loans in the UAE

Theres a plethora of notable business loan types available that you should consider before deciding on one to quickly secure your funds

Source: UAE Central Bank; Islamic finance institution product terms; UAE SME loan programme documentation.

[blockCTABizActivityList]

Eligibility Criteria for Loan Application in UAE

Getting instant approval from the lending institution can be a bit of a challenge unless you meet most of the crucial eligibility criteria. Banks in Dubai are quite particular about accepting a loan application, with a major focus on previous financial history and availability of funds.

Here are some of the basic criteria for applicants;

- Being at least 21 years of age.

- The business should have been operating for at least a year this is because a time period less than that would not provide substantial proof of profit and loss statements to make sure that the business has enough liquidity to pay upcoming instalments.

- Have a proper corporate bank account.

- Effective presentation of bank account statements for the past 6 to 12 months.

- Although it varies from bank to bank, the yearly sales revenue should amount to at least AED 1 million to receive the loan.

- If your company is set up as a subsidiary or an offshore branch company, obtaining a business loan may be easier due to the diversity of operations and the need for larger funds.

Having a corporate bank account is one of many eligible requirements you need to have, and with Meydan Pay, setting up your business bank account will be as convenient as it gets.

You can choose from our banking partners who have a range of foreign and local currencies to aid payments and unparalleled banking services, all whilst accessing your accounts on an interactive, digital platform.

[blockExpertOpinion]

Requirements for Business Loan Applications in UAE - Documents Required

Theres an extensive documentation process that you need to carefully follow to get approval from the bank you desire. You have to obtain the relevant business license and collate the needed paperwork to be accepted.

A general trade license is vital to operate your business in the UAE. At Meydan Free Zone, you can access over 2500 business licenses that suit various business activities, at some of the most affordable bundle costs.

Heres a list of the documents you need to prepare;

- Trade License

- Bank application

- Passport copy of loan applicant

- Bank statements from the past 6 to 12 months

- Copy or original of Articles of Association

- Copy or original of Power of Attorney

- Copy or original of Memorandum of Association.

- Home residence tenancy agreement.

- Audit reports.

- List of employees from the Ministry Of Labour.

- VAT certificate copy

Things to Know Before You Apply for a Loan in UAE

Before you apply for a loan in the UAE, there are some pointers regarding finance procedures you need to have adequate knowledge on. This can help you improve your eligibility score and meet other requirements.

[blockFaqsCategory]

[blockCTACostCalculator]

Benefits of Applying for a Business Loan in Dubai

After reading the aforementioned information, we can gather that loan application in Dubai consists of certain benefits like;

- Assistance to prepare essential documentation - Economic jurisdictions like Meydan Free Zone specialise in helping you set up your new business with optimum ease, which includes eliminating irritating paperwork.

- Loan amounts can reach up to AED 5 - 7 million.

- Loan types are available for SMEs, large enterprises, startups and business models of all sorts.

- Flexible repayment plans and tenures

[blockCTANameCheck]

Why Meydan Free Zone?

Meydan Free Zone is located in the heart of Dubai, surrounded by the skyscrapers that shape the city’s iconic skyline. With stunning views, world-class hospitality, and seamless transport links to seaports and airports, it has become a hub that attracts ambitious start-up entrepreneurs ready to achieve their goals. With access to residency support and banking support, businesses can establish a strong foundation from the very beginning.

There is no doubt that every business needs the right financial backing to succeed. Financial stability sits at the centre of all business decisions and future planning, influencing operational risks, marketing strategies, and human resource management. Maintaining strong financial health is essential for long-term growth and sustainability.

Not sure where to start? Calculate your business setup costs today and take the first step towards building a financially secure future.

Contact us for further inquiries!

Citations

1 Arab News, citing Central Bank of the UAE.. UAE SME loans and commercial credit data, H1 2024. Arab News, 2024.

2 Central Bank of the UAE.. Quarterly Economic Review — SME Credit Data. Central Bank of the UAE, 2024.

3 UAE Ministry of Economy.. SME Sector and Business Loan Support Programmes. UAE Ministry of Economy, 2024.