Table of Contents

Frequently Asked Questions

1. How can an Indian entrepreneur open a business bank account in Dubai?

You can open a business bank account in Dubai after receiving your trade license. Submit your passport, company license, KYC details and a short description of your business model. Free zones like Meydan Free Zone offer a guided IBAN pathway that speeds up approval.

2. How long does it take to open a corporate bank account in Dubai?

With a complete file, many UAE banks can issue an IBAN in around one working day when onboarding through Meydan Free Zone. Full activation follows once compliance checks are completed.

3. Can I open a Dubai business bank account without visiting the UAE?

Some banks allow remote onboarding, but others may require an in-person verification depending on your business activity and risk profile. Many Indian founders begin the process remotely and travel only if needed.

4. Why do UAE banks ask about my business activity?

UAE banks assess risk based on what your company actually does. Clear, well-defined business activities make onboarding faster. Free zones like Meydan Free Zone offer 2,500+ precise activity options, which helps banks verify your profile quickly.

5. Is Dubai business banking easier for consultants and service companies?

Yes. Consulting, IT services, marketing, advisory and other service-led companies usually experience smooth onboarding because their activities are simple to verify and involve predictable financial flows.

6. Do Dubai banks accept Indian companies and founders easily?

Yes. Indian entrepreneurs are among the largest business groups in Dubai. Banks regularly onboard Indian-owned companies, especially when the business model is clear and the license is issued by a reputable free zone.

Topic Summary

1. Streamlined Account Opening Process

Unlike India’s complex documentation requirements, Dubai offers a more straightforward account opening process, often requiring basic KYC documents, such as passport copies, visa details, and proof of business registration, enabling faster onboarding.

2. Multiple Currency Facilities

Dubai banks provide multi-currency accounts, allowing Indian entrepreneurs to hold and transact in various currencies—including AED, USD, and INR—helping to manage foreign exchange risks and simplify cross-border transactions.

3. Dedicated Relationship Managers

Banks in Dubai assign experienced relationship managers who understand the specific needs of expatriate business owners, offering personalized support to navigate banking services efficiently and ensure smooth operations.

4. Robust Digital Banking Solutions

Most Dubai banks offer advanced online and mobile banking platforms with features tailored for businesses, enabling easy fund transfers, salary payments, and real-time account monitoring without the need for frequent branch visits.

5. Access to Trade Finance and Business Loans

Dubai’s banking sector provides various financial products such as trade finance, working capital loans, and credit facilities designed to support business growth, helping Indian entrepreneurs secure the necessary funds to expand confidently.

Business Banking Made Simple For Indians Setting Up in Dubai

If you ask any Indian entrepreneur what scares them most about expanding abroad, nine times out of ten they’ll say “banking.” Not taxes. Not licensing. Not compliance. Banking.

And understandably so. In India, opening a current account can feel like a rite of passage - a long dance involving address proofs, GST filings, cancelled cheques, relationship managers, and more documents than your CA wants to admit exist.

Dubai flips this experience on its head.

Not because it's lax, far from it. The UAE has one of the most robust AML and compliance frameworks in the region.

The CBUAE 2025 Annual Report shows the UAE banking sector reached AED 5.4 trillion in total assets, with 17.9% credit growth and 16.2% deposit growth year-on-year, while licensed fintech companies more than doubled to 36 over the same period.¹

Behind that scale sits a system the country builds deliberately: digital, predictable, rule-based. The result? Business banking in Dubai feels less like a hurdle and more like part of a smooth onboarding experience.

For Indian founders expanding into Dubai, this becomes one of the biggest pleasant surprises.

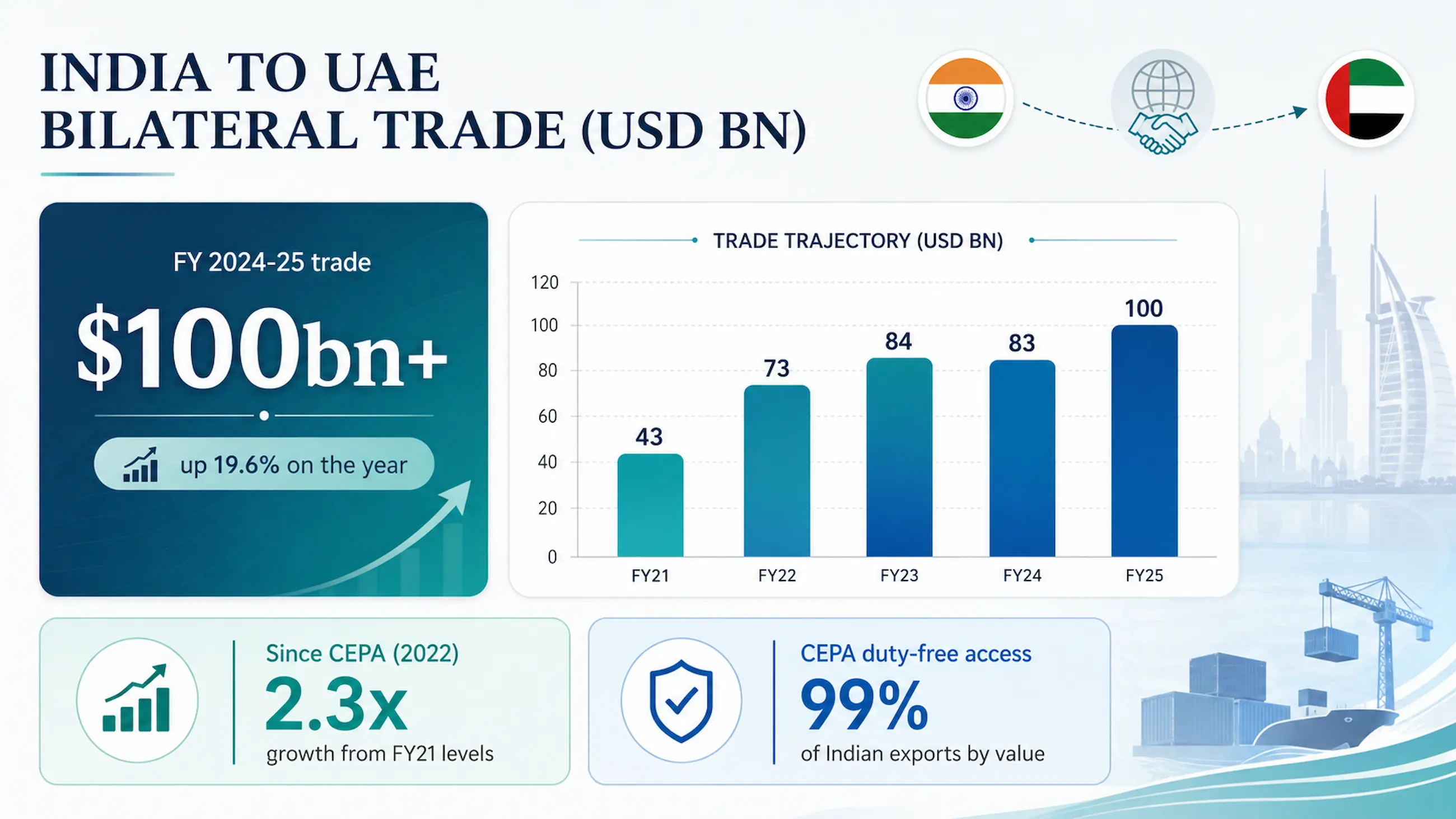

A Dubai business account is not opening into a vacuum. It connects you to an India-UAE trade relationship that crossed USD 100 billion in FY 2024-25, which is a large part of why UAE banks are so practised at onboarding Indian founders.

Sources: DD News / Government of India (2025); Middle East Briefing (2025).

Why Banking Feels Different in Dubai (Especially When You’re Coming From India)

India conditions entrepreneurs to expect friction. KYC is repetitive, branch visits are normal, signatures and stamps multiply, and even after you submit everything, approval timelines can feel ambiguous.

Dubai is structured differently.

UAE banks want clarity, not paperwork overload. They care about:

- Who owns the company

- What the company actually does

- Where money will come from and go

- Whether the business activity aligns with the license

- Your cross-border flow expectations

That’s it.

No obsession with utility bills. No stamp-paper affidavits. No hardbound bank statements.

The UAE Central Bank enforces strict compliance norms, but they are transparent and rule-based, not interpretative.

This clarity is why thousands of Indian-owned companies now operate financial structures across India + UAE seamlessly.

[blockCTACostCalculator]

The Business Banking Process for Indians in Dubai: What Actually Happens

The bank account usually opens after your company license is issued, and this is where choosing the right free zone changes everything.

Free zones that maintain strong governance standards, digital processes and MoFA-accredited documentation tend to be trusted by banks. Meydan Free Zone happens to be one of them, and this directly impacts your banking experience.

Once your trade license is active, you submit your Company profile, along with Authorised Signatory Details, such as:

- Emirates ID

- Proof of residence

- Personal bank statement (6 months)

- CV

There is no requirement for Indian financial statements, GST returns or income tax documents unless your specific case calls for additional review.

And here’s the part Indian founders appreciate most:

When you set up through Meydan Free Zone, you get access to a guaranteed IBAN pathway through partner banks. This means your application is sent through an internal, priority-reviewed channel rather than the cold “apply-and-hope” method many Indian founders use when approaching UAE banks on their own.

That simple shift, structure over uncertainty, removes the fear Indian entrepreneurs have about banking delays.

Why UAE Banks Ask Different Questions Than Indian Banks

Indian banks typically start with paperwork volume. UAE banks start with business logic.

This isn’t interrogation, it’s risk profiling, and it’s globally standard. The UAE simply executes it with more transparency and less noise.

This is also why selecting the right business activity matters so much. If your business license clearly shows what you do, banks are far more comfortable. Free zones like Meydan, which offer 2,500+ activities, make it easier to choose a precise match.

[blockCTANameCheck]

How Long Does Business Banking in Dubai Actually Take?

Most Indian founders assume banking takes weeks. In reality, with a complete file and a well-matched business activity, Meydan Free Zone’s banking partners can issue an IBAN in around one working day after all documentation is submitted.

The account becomes fully active once final bank checks are completed, but the speed at which you receive your IBAN shocks most Indian entrepreneurs — in a good way.

This is possible because the UAE banking system is deeply integrated with digital onboarding and pre-screened partner ecosystems.

Which Types of Indian Businesses Find UAE Banking Easiest?

Banking is smoother when the business model is transparent and service-led. Indian entrepreneurs running:

- Tech consulting

- Digital services

- SaaS or IT solutions

- Tax or compliance advisory

- E-commerce

- Professional consulting

- International trading with clear supply chains

…generally experience faster approvals because their activity descriptions are clear, globally recognisable and aligned with standard compliance checks.

But even more traditional businesses - textiles, manufacturing export, wholesale distribution - now enjoy easier onboarding compared to a few years ago because UAE banks have become familiar with India - UAE trade patterns under CEPA.

[blockCTAmAccounting]

Why Meydan Free Zone Makes Banking Simpler for Indians

Meydan Free Zone is one of the rare free zones that is:

- fully digital,

- MoFA-accredited anbd Dubai Chamber-accredited

- and integrated with a banking partner network that understands Indian founders.

This matters because banks look at two things:

- The credibility of the licensing authority

- The clarity of your business model

Meydan Free Zone’s governance, recognition and 2,500+ activity structure check the first box.

Your service scope checks the second.

Together, they reduce uncertainty and create a smoother onboarding experience.

You can explore banking and licensing support through the Meydan Free Zone or book a consultation

Digital Banking, Payment Gateways and the Modern Indian Founder

Most Indian entrepreneurs expanding to Dubai are digital-first. They want to operate lean, invoice globally, and accept online payments.

The UAE supports this ecosystem through:

- robust fintech adoption,

- e-KYC integration,

- multi-currency accounts,

- and payment gateways tuned for regional and international commerce.

However, payment gateway onboarding still depends on precise business activities and a clean corporate structure. This is another reason why choosing the right free zone - and the right business activity description - matters more than people assume.

A trader with unclear HS classifications or a consultant with a vague license will slow onboarding.

A clean, precise setup accelerates everything.

[blockCTAContact]

Business Banking in Dubai Is Not Complicated - It’s Conditional

For Indian founders, the fear of Dubai banking usually comes from imagining an India-like experience. But the UAE operates on clarity, not friction. When your company is licensed through a strong free zone, your activities are clearly defined, and your business model is transparent, banking becomes one of the easiest parts of your Dubai expansion.

A system that values structure over bureaucracy becomes a system entrepreneurs can trust.

If you’re planning to set up a Dubai entity - and want a banking experience that feels predictable rather than painful - you can explore your options with Meydan Free Zone.

Dubai may be a new market.

But its banking system speaks the language Indian founders understand: clarity, speed, and global ambition.

Citations

¹ Central Bank of the United Arab Emirates, "CBUAE 2025 Annual Report," April 2026.