Table of Contents

Frequently Asked Questions

What is the French exit tax when moving to Dubai?

French exit tax can apply when a French tax resident leaves France with company shares that have increased in value, even if those shares have not been sold.

Who does Article 167 bis apply to?

Article 167 bis can apply to French tax residents who lived in France for six of the last ten years and hold shares over €800,000 or 50% of a company.

Can French exit tax be deferred when moving to Dubai?

Yes. For a Dubai move, French exit tax can usually be deferred if the founder declares the gains, requests deferral, appoints a representative and provides required guarantees.

Can you set up a Dubai company before leaving France?

Yes. With Meydan Free Zone, French founders can set up a Dubai company remotely before relocating, so the UAE business base is ready when exit-tax timing is clean.

How does Meydan Free Zone help French founders moving to Dubai?

Meydan Free Zone helps founders set up a Dubai company, choose activities, access banking pathways, apply for residency, prepare TRC documents and maintain compliance records.

Topic Summary

1. Understanding the Exit Tax Framework

Under French tax law, the exit tax targets unrealised gains on company shares when a taxpayer leaves France. Unlike conventional capital gains tax, this tax applies not to cash holdings but on the paper value of shares, effectively taxing potential future profits as if they were realised at the point of expatriation.

2. Criteria for Application Under Article 167 bis CGI

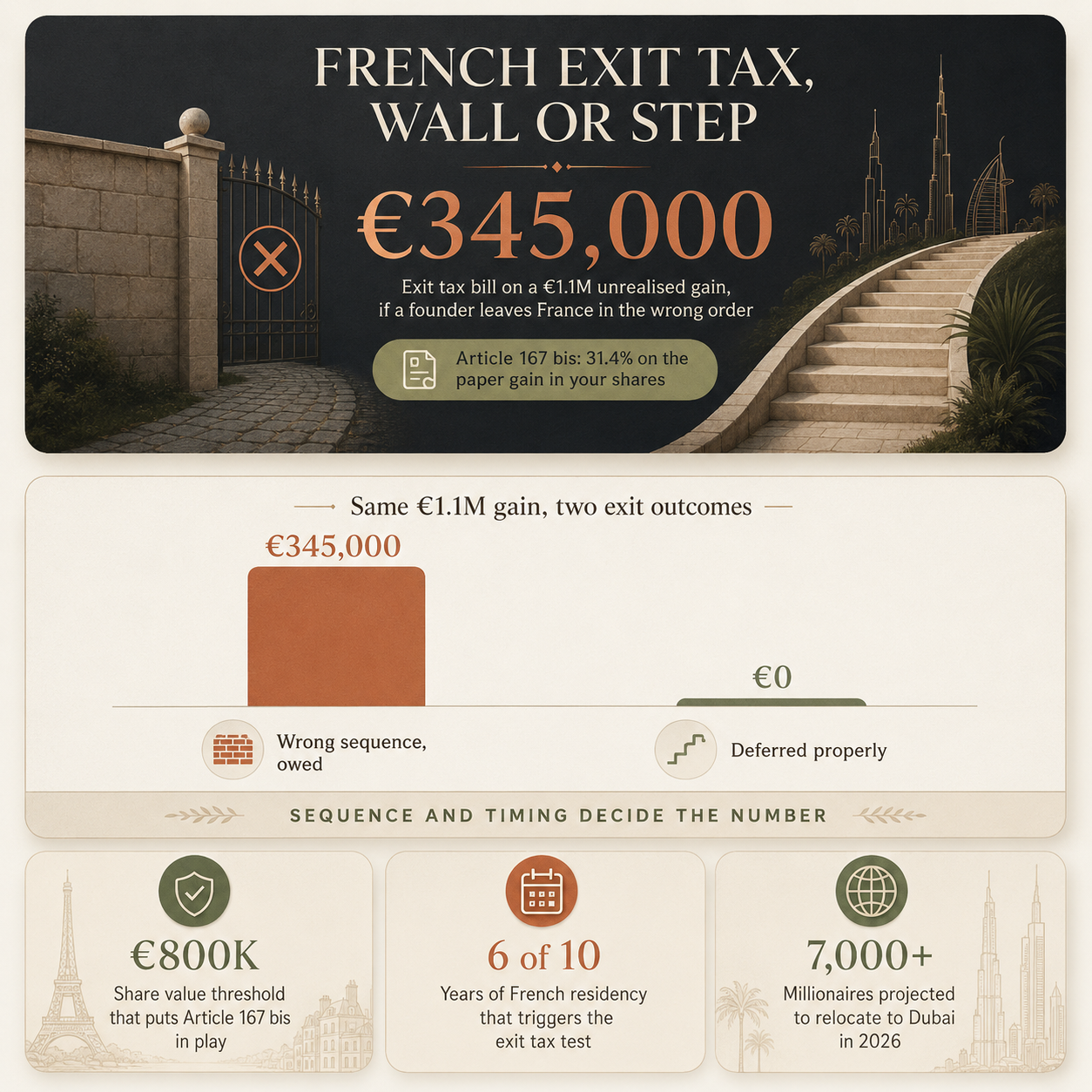

Article 167 bis of the French General Tax Code (CGI) stipulates that this exit tax may apply if an individual has been a French tax resident for at least six of the previous ten years and owns shares with a valuation exceeding €800,000. Alternatively, the tax also applies if the individual holds more than 50% of the voting rights or capital in a company, irrespective of the €800,000 threshold.

3. Scope and Valuation of Taxable Shares

The taxable amount is calculated based on the market value of shares on the day residency ceases, reflecting not actual cash proceeds but the hypothetical gains at departure. This valuation can encompass all entities controlled directly or indirectly, potentially creating a substantial tax liability for founders with sizeable equity positions.

4. Strategic Considerations for Founders Planning Relocation to Dubai

Dubai, ranked by Henley & Partners as the leading global destination for relocation, offers significant tax advantages for expatriates. However, meticulous planning is essential to manage exit tax obligations. French founders should consider timing their departure, shareholding structure optimisation, and possible deferrals or payment spreads to mitigate immediate tax impact.

5. Compliance and Professional Advisory Imperative

Given the complexity of Article 167 bis, it is critical for French founders contemplating relocation to Dubai in 2026 to seek expert legal and tax advice. Proper compliance ensures that exit tax liabilities are lawfully addressed while maximising the financial

Exit Tax & Article 167 bis CGI: The French Founder's 2026 Guide to Leaving for Dubai the Right Way

France can tax you on money you have not made yet. Not cash in your account, but the paper value of your company shares, taxed when you leave.

This is the exit tax. Under Article 167 bis, it can apply if you have been French tax resident for six of the last ten years and hold shares worth over €800,000, or more than 50% of a company.

Henley & Partners ranked the UAE as the world’s top destination for relocating millionaires in 2025, attracting around 9,800.¹ Its 2026 report expects Dubai to add over 7,000 more this year.²

The good news is that the exit tax is not a wall. For a Dubai move it can usually be deferred, and often cancelled entirely, with the right timing. So French exit tax when moving to Dubai is the first thing to plan, and part of that is having your base ready: Meydan Free Zone sets up your company remotely and licensed in under 60 minutes, so residency follows when the timing is right.

[blockCTAFawri]

Will The French Exit Tax Catch You?

The French exit tax, under Article 167 bis, works on a simple idea: if your company grew in value while you were a French tax resident, France wants to tax that gain, even if you have not sold a thing. Move your tax residence abroad and it treats the rise in your shares as if you had cashed it in, taxing the paper gain at the standard 31.4% rate.

What the Exit Tax Could Cost a French Founder

Take a founder who owns 60% of a French company worth €2 million:

- Shares worth €1,200,000 at departure

- Original cost of €100,000

- An unrealised gain of €1,100,000

Nothing has been sold. No cash has changed hands. But move your tax residence out of France, and Article 167 bis can treat that €1.1 million paper gain as taxable the day you leave.

At the headline 31.4% rate, that is roughly €345,000, before any reliefs or surtaxes.

Source: French General Tax Code Article 167 bis and BOFiP guidance, PwC France Individual Taxes 2026, and Henley & Partners Private Wealth Migration Report 2026, via BOFiP France

Do You Actually Pay the Exit Tax When You Leave?

For a move to Dubai, the exit-tax bill does not always have to be paid on departure.

[blockFaqsCategory]

Setting Up Your Dubai Base with Meydan Free Zone Before You Leave

Deferral is handled on the French side. But the move still needs somewhere real to land, and that is where Meydan Free Zone fits.

You do not have to wait until you leave France to prepare it: the company can be set up remotely first through Meydan Free Zone’s 24/7 digital portal, so the UAE base is ready the moment your exit-tax timing is clean.

How to Plan Your Exit From France to Dubai

[blockAccordionSteps]

[blockCTATradeLicense]

In Conclusion

Everything about leaving for Dubai comes down to sequence. The founders who get caught out are the ones who move first and look at the exit tax afterwards, when the options have already narrowed.

Do it the other way round, review the position, defer in time, set up the Dubai side, then move, and the tax that looks like a wall becomes a step you plan through.

If you are planning around the French exit tax when moving to Dubai, book a free consultation with a setup advisor at Meydan Free Zone to build your Dubai company in the right order, with the activity scope, banking path and residency route ready before you leave.

Citations

¹ Henley & Partners, Private Wealth Migration Report 2026, UAE the top destination for relocating millionaires in 2025, June 2026.

² Henley & Partners (via Haute Living), The Wealthiest Map of the World Has Just Been Redrawn, Dubai projected to add over 7,000 millionaires in 2026, April 2026.