Table of Contents

Frequently Asked Questions

1. Can a Chinese entrepreneur open a UAE bank account without a residence visa?

No. A stamped UAE residence visa is mandatory before any personal account process starts. For a corporate account, you need an active Trade License and Establishment Card. Approaching any bank before these are in place results in a wasted visit and restarts the compliance clock.

2. How long does it take to open a corporate bank account in Dubai for Chinese investors?

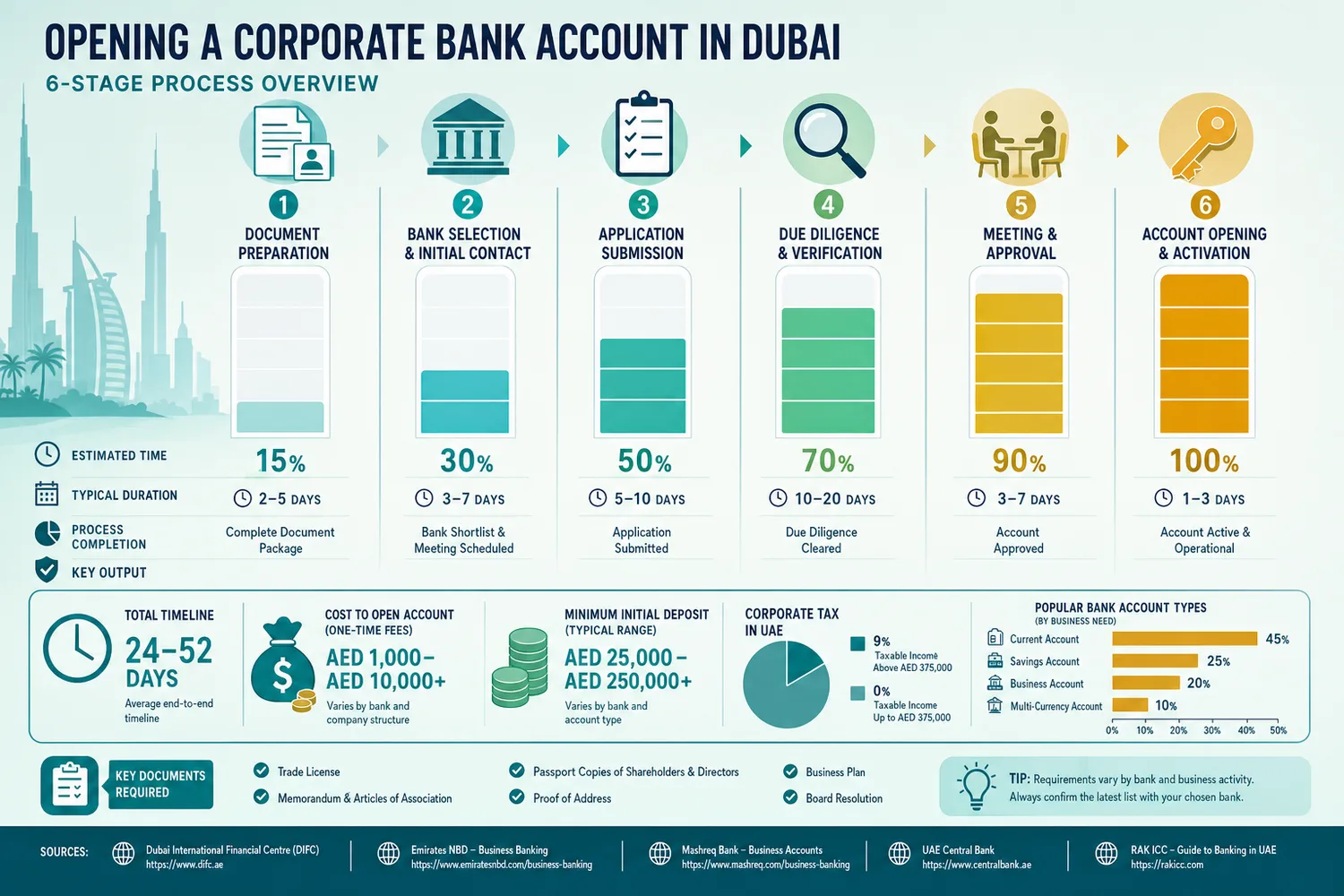

Allow 2–6 weeks from document submission to activation appointment. Standard processing runs three to seven business days for a fixed case, but compliance review can extend the timeline significantly. Chinese New Year and UAE public holidays can add further delays.

3. What source of funds documentation do UAE banks require from Chinese applicants?

UAE banks operate under strict anti-money laundering (AML) and Know Your Customer (KYC) requirements. Chinese applicants must provide three to six months of bank statements translated into English, showing salary, dividend income, or business revenue consistent with the declared source of funds.

4. Is a Free Zone or Mainland company better for banking as a Chinese entrepreneur in Dubai?

Free Zone companies with clear digital or trading-focused license activities are generally processed faster by compliance teams. Mainland company is the appropriate structure if you want to trade directly within the local UAE market, take on government contracts, and operate from any location, but attracts more extensive compliance review.

5. Do Chinese entrepreneurs need to report UAE bank accounts or income to Chinese tax authorities?

China taxes residents on worldwide income, and the UAE-China double tax treaty governs how income is taxed in both jurisdictions. Seeking specialist advice from a cross-border adviser before you proceed is not optional, this is the most common error Chinese founders discover too late.

Topic Summary

1. Gather Documents Before Approaching Any Bank

UAE banks need a real business story, account applications without documented client contracts and projected annual revenue rarely gets approval. Have your Trade License, Establishment Card, Memorandum of Association, and source of funds statements ready before booking any appointment.

2. Free Zone or Mainland Affects Your Banking Profile

Free Zone companies with clear license activities often move through compliance review faster than Mainland companies regulated by the Department of Economic Development. The decision that determines cost and banking profile is made at the jurisdiction stage, not the bank stage.

3. Source of Funds Is the Compliance Point Most Miss

UAE banks operate under strict anti-money laundering (AML) and Know Your Customer (KYC) requirements. Prepare three to six months of Chinese bank statements translated into English, large transfers without documentation trigger enhanced due diligence and create personal liability.

4. Corporate Accounts Take Two to Six Weeks

The compliance review process is not same-day, allow two to six weeks from document submission to activation appointment. A corporate bank account can add another two to four weeks onto the total setup timeline if founders treat banking as an afterthought, creating signed contract financial consequences.

5. Personal Accounts Start From Residency Stamping

The timeline is triggered by the visa stamp date, not Emirates ID collection. Chinese entrepreneurs can begin a personal account process immediately using the ICP application receipt before the physical card arrives.

6. License Activity Must Match Your Business Profile

A license activity mismatch, registering 'general trading' but describing tech consultancy, creates a compliance flag that can run from two to four weeks to resolve. Banks cross-reference the Trade License activity against every document submitted.

7. Chinese Tax Exit Obligations Are Not Optional

China taxes residents on worldwide income, and the UAE-China double tax treaty governs how income is taxed in both jurisdictions. Seeking specialist advice to address Chinese tax exit obligations before the process starts, not as a parallel task, is the most common error Chinese founders discover too late.

Open Corporate & Personal Bank Accounts in Dubai for Chinese Expats

Chinese entrepreneurs represent one of the fastest-growing segments of new business registrations in Dubai, yet the bank account opening process stops more of them cold than any other part of the setup. The compliance requirements are real, the documentation burden is heavier than most expect, and the founders who sail through are those who treat banking as part of the company formation sequence from day one. This guide covers what UAE banks actually require, how to prepare correctly, and what the compliance process looks like in practice.

What You Need Before Approaching Any Bank

Opening a Dubai bank account for Chinese entrepreneurs starts well before you walk into any branch. You need a valid, active Trade License, an Establishment Card (Immigration File), a stamped residence visa, and a Memorandum of Association confirming ownership structure. Without the Establishment Card, the bank's compliance team has no Immigration File reference to work with, the process stalls immediately.

For personal accounts, the trigger is the residence visa stamp date, not Emirates ID collection. You can start the application using an ICP application receipt while the physical card is still being processed. Proof of address, a tenancy contract or utility bill, and three to six months of Chinese bank statements translated into English are mandatory.

The Business Story Requirement Most Founders Miss

UAE banks need a real business story. An account application without signed client contracts and projected annual revenue rarely gets approval. Prepare a concise business profile covering your license activity, target markets, and key clients. A company website or verifiable digital presence supports the compliance officer's review. Chinese investors with Dubai banking applications should translate key documents into English or Arabic before submission, incomplete submissions cause delays, not just inconvenience.

Free Zone vs. Mainland: What It Means for Banking

Free Zone companies with clean, digital-focused license activities generally move through compliance review faster than Mainland structures. The license activity determines what transaction flows the bank expects to see, a mismatch between stated activity and actual cash flows triggers enhanced due diligence. A Guangzhou trading company with a Mainland license faces a more detailed review than a Chengdu tech consultant operating through a Free Zone with international clients.

Meydan Free Zone offers a digital setup process and trading-friendly license structures well suited to Chinese entrepreneurs whose business model doesn't require a physical UAE storefront. Free Zone structures keep setup costs lower through mandatory virtual or flexi-desk arrangements, and the banking profile is typically cleaner.

How to Open a Corporate Bank Account: Follow This Sequence Precisely

Source of Funds: The Compliance Point Most Chinese Applicants Underestimate

UAE banks operate under strict anti-money laundering (AML) and Know Your Customer (KYC) requirements. Large initial transfers from China will trigger enhanced due diligence, have documentation ready before the transfer, not after. A Guangzhou business owner planning to transfer AED 200,000 as initial capital should prepare dividend records, tax filings, and bank statements showing a clear, consistent funds trail.

- Prepare dividend records, tax certificates, and bank statements showing a clear, consistent source of funds before initiating any transfer

- Document the full chain of funds, from business income in China through to the amount being transferred to the UAE

- Ensure all documents are translated into English or Arabic by a certified translator

- Avoid round-number transfers without supporting documentation, as these are more likely to trigger enhanced due diligence reviews

- Be ready to explain the nature of the business, the reason for the transfer, and the intended use of funds in the UAE

- Keep records of any previous international transfers, as UAE compliance officers may request a broader financial history

- Engage a UAE-based financial adviser or corporate services provider before the transfer, not after questions arise

China Tax Residency: Address This Before You Proceed

China taxes residents on worldwide income. Chinese entrepreneurs who relocate to Dubai but maintain significant ties to China may remain tax resident in China for reporting purposes. The UAE-China double tax treaty governs how income is taxed in both jurisdictions, and seeking specialist advice from a cross-border adviser before you proceed is not optional. Addressing Chinese tax exit obligations before the process starts, not as a parallel task, is the most common error Chinese founders discover too late.

What to Do This Week

Define your license activity and choose jurisdiction first. Gather your documents, passport copies, translated Chinese bank statements, signed client contracts. Contact a cross-border adviser to address Chinese tax obligations. Use the Meydan Free Zone Setup Cost calculator to get a detailed cost breakdown before committing to any structure.

Opening a Dubai bank account for Chinese entrepreneurs is a structured process with clear prerequisites. Get the corporate structure right, prepare source of funds documentation before approaching any bank, and build four to six weeks into your timeline for a complete, functional setup.