Table of Contents

Frequently Asked Questions

1. Can a German entrepreneur open a UAE corporate bank account without a residence visa?

No. UAE banks need a stamped residence visa alongside the Trade License, Immigration File, and Emirates ID in process before they will review a corporate account. A founder with only a Trade License and no residence visa faces rejection, the process isn't automatic after company setup.

2. How long does it take to open a corporate bank account in Dubai for a German founder?

Once all prerequisites are in place, onboarding runs five to ten business days for standard cases. Mashreq Neo Business typically runs five to seven business days; Emirates NBD runs seven to ten. Incomplete submissions cause delays, confirm the exact document list before booking.

3. What is the minimum balance for a UAE corporate bank account?

Minimum balance obligations aren't one-size-fits-all. Emirates NBD runs AED 50,000–100,000 for corporate accounts; Mashreq Neo Business runs AED 25,000. Confirm the exact threshold before proceeding, falling below it triggers a monthly price that erodes working capital.

4. What documents does a UAE bank need from a German entrepreneur for a corporate account?

UAE banks need a real business story: Trade License, Establishment Card, Memorandum of Association, colour copy of the passport, high-quality photograph with a white background, Emirates ID in process, projected annual revenue figures, and signed client contracts. A vague business activity rarely gets approval.

5. Do German entrepreneurs need to address German tax exit obligations before opening a Dubai bank account?

Yes, this is what most German founders discover too late. A founder who has not formally completed their German tax exit before opening a UAE corporate bank account risks being taxed in both jurisdictions. Seeking specialist advice from a cross-border adviser before the process starts is not optional.

Topic Summary

1. Get the Foundation Right First

A valid Trade License and opened Immigration File are non-negotiable before any UAE bank will review a corporate account process. The account will be refused without both in place, it isn't automatic after company setup.

2. UAE Banks Need a Real Business Story

Projected annual revenue figures, a signed contract, and Emirates ID in process or being compiled are standard submission obligations. A vague business activity rarely gets approval, incomplete submissions cause delays.

3. Choose the Right Bank for Your Model

Emirates NBD suits international founders with relationship banking needs; Mashreq Neo Business offers digital-first onboarding with a lower minimum balance. Falling below the exact threshold triggers a monthly price that erodes working capital.

4. Follow This Sequence Precisely

Trade License first, Immigration File second, Entry Permit third, then in-country residency steps, each step unlocks the next. A founder who books a bank appointment before the Immigration File is opened and functional will find the entire process stalls.

5. Free Zone Is Often a Perfect Fit

A Free Zone corporate setup allows 100% foreign ownership, packages tailored to consultants and tech entrepreneurs, and operate from any location. Mainland company is the appropriate structure only when direct UAE market access is mandatory.

6. Address German Tax Exit Before Banking

A founder who has not formally completed their German tax exit before opening a UAE corporate bank account risks being taxed in both jurisdictions. The UAE structure delivers no tax benefit in that scenario, seeking specialist advice before the process starts is not optional.

7. Most Expats Discover Too Late: Compliance Gaps Cost Time

Health insurance is mandatory under UAE residency rules, and banks monitor residency status as part of ongoing KYC obligations. A German founder who lets their residence visa lapse will find their corporate bank account subject to compliance review.

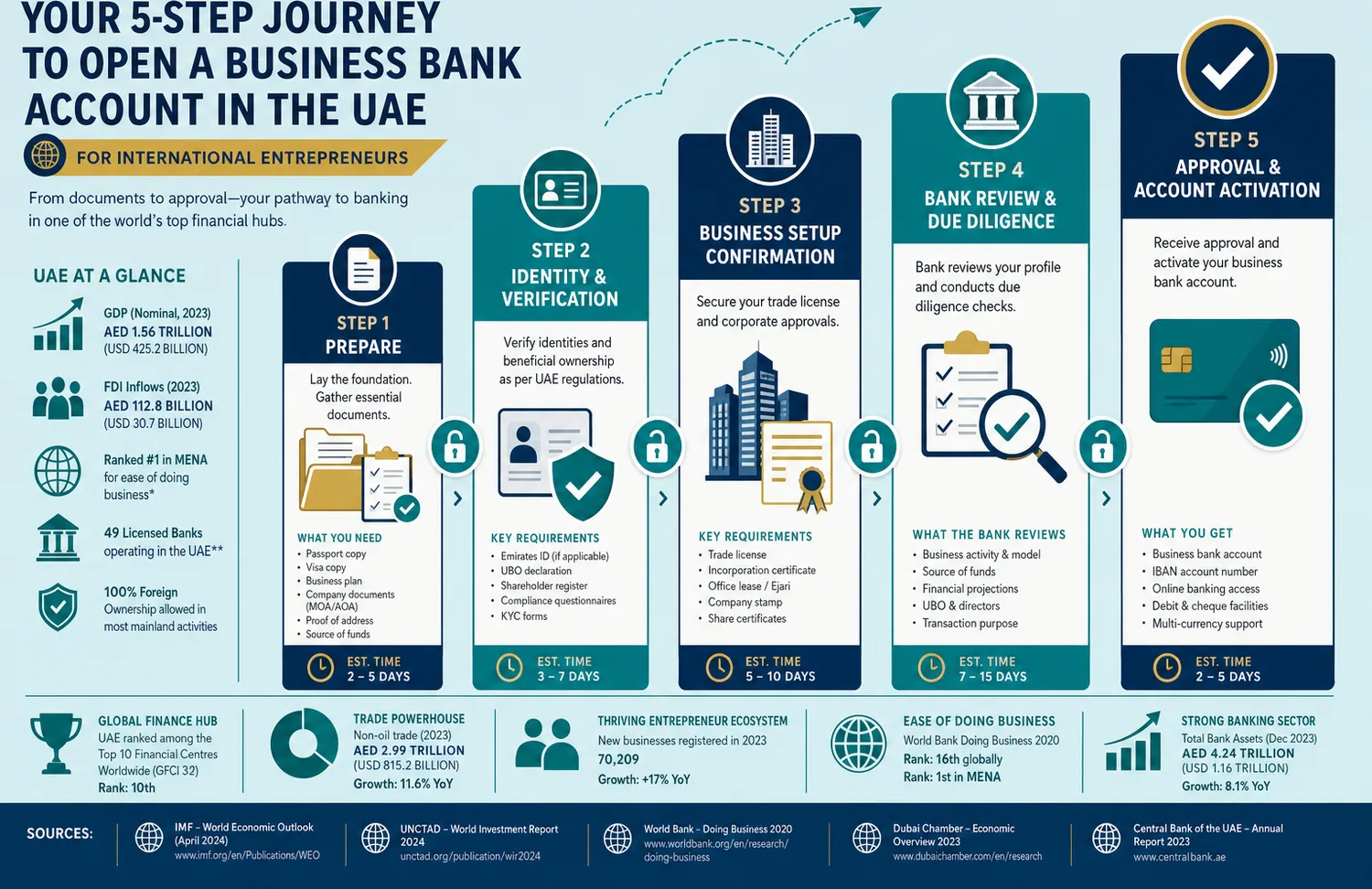

Corporate and Personal Banking in Dubai for German Entrepreneurs

German entrepreneurs setting up in Dubai often assume the hard part is company setup. It isn't. The harder part is getting a Dubai bank account for German entrepreneurs approved and active, and most founders discover this too late, after the Trade License is issued and the Immigration File is sitting idle.

The Trade License is the foundation, without it, no corporate process starts. A stamped UAE residence visa is mandatory for personal account opening and strongly favoured for corporate accounts. The Establishment Card, confirming the corporate entity exists in the UAE system, must be up and running before any bank will treat the entity as commercially real. The Emirates ID in process or being compiled is accepted at most banks.

What UAE Banks Require from German Entrepreneurs

UAE banks need a real business story. So having only a Trade License and no residence visa faces rejection. The same founder with documented client contracts, projected annual revenue, and the ICP application receipt proceeds without any test of patience.

These typically include:

- Trade License (original, unexpired) and Memorandum of Association, incomplete submissions cause delays

- Establishment Card, confirming the corporate entity exists in the UAE system

- A clear, colour copy of the passport with at least six months' validity

- A need a high-quality photograph with a white background

- Emirates ID in process or being compiled, the physical card does not need to be stamped

- Signed client contracts and projected annual revenue documentation

- A local UAE address, a flexi-desk arrangement satisfies this obligation

- Some banks require a professional email, phone number ready, and a summary of projected annual revenue

Choosing the Right Bank

NBD, ADCB, and Mashreq are the most commonly used options. Each has different minimum balance thresholds, confirm the exact threshold before proceeding. Falling below triggers a monthly price that erodes working capital.

How to Open a UAE Corporate Bank Account

Each step unlocks the next, skipping any one of them stalls the entire process. The UAE corporate bank account process isn't automatic after company setup.

Confirm the Trade License is valid and the Immigration File is activated first. A founder who books a bank appointment before the Establishment Card is fully activated will find the account will be refused; it isn't automatic after company setup.

Submit everything, Trade License, Establishment Card, Memorandum of Association, passport copies, Emirates ID in process receipt, and projected annual revenue documentation. The account is not functional until the bank completes its AML and KYC review. Compliance Review and Account Activation is not same-day, allow five to ten business days. This gives you a functional UAE corporate account with a UAE IBAN before the first transaction clears.

Corporate Tax and VAT Reporting Obligations for German Founders

As of June 2023, a federal Corporate Tax of 9% applies to taxable profits exceeding AED 375,000 annually. VAT at 5% is mandatory for businesses with annual revenues over AED 375,000. Your business is compliant when you register for Corporate Tax and VAT Reporting Obligations from day one.

A German founder who has not formally exited German tax residency before opening a UAE corporate bank account will find their UAE income potentially assessable by German tax authority, the UAE structure delivers no tax benefit in that scenario. Seeking specialist advice to address German tax exit obligations before the process starts is not optional.

Most Expats Discover Too Late: Compliance Consequences

UAE banks need a clear commercial activity because vague or high-risk activity rarely gets approval. The Establishment Card must be fully activated before any bank will treat the entity as commercially real.

A German founder who books a bank appointment two days after the Trade License is issued will find the entire process stalls. Health insurance is mandatory as a required condition of UAE residency, failing to maintain health insurance creates a compliance gap that can affect visa renewal and indirectly banking status.