Table of Contents

Frequently Asked Questions

1. Can you keep your assurance-vie when moving to Dubai?

Yes. You can usually keep your assurance-vie after moving to Dubai, but withdrawals, beneficiary clauses, insurer records and non-resident tax treatment should be reviewed with a French adviser before withdrawals.

2. Can you keep your PEA after leaving France for Dubai?

Yes. A PEA can generally stay open after you leave France for Dubai, since the UAE is not on France’s non-cooperative tax list, but new PEAs usually require French residence.

3. How is a PEA taxed after moving abroad?

For French non-residents, PEA gains are generally outside French income tax and social charges when withdrawn, provided the plan remains valid and withdrawal rules are followed under French tax rules.

4. Does Dubai tax assurance-vie or PEA gains?

No. The UAE does not levy personal income tax or capital gains tax at the UAE level, so Dubai adds no extra tax layer on French investment gains for residents.

5. How does Meydan Free Zone help French savers moving to Dubai?

Meydan Free Zone helps build the Dubai side: company setup, residency, Emirates ID, corporate banking support, accounting records and Tax Residency Certificate preparation once you qualify as a resident properly.

What Happens to Your Assurance-Vie & PEA When You Move to Dubai?

Leaving France does not mean closing your assurance-vie or your PEA.

That is the fear most French savers have, that the move abroad destroys their two big tax-friendly wrappers. It does not. In most cases you keep both, and Dubai turns out to be one of the best places to hold them.

The assurance-vie is a life-insurance savings wrapper, holding around €2.1 trillion in France, according to France Assureurs.¹ The PEA is a share-savings plan. Both let your money grow with light tax while it stays invested.

What changes when you move comes down to three questions: can you keep it, how does France tax it now, and does Dubai tax it too? For a French assurance-vie or PEA, moving abroad changes less than most people fear. You keep both, France taxes you more lightly as a non-resident, and per PwC, Dubai adds no tax of its own.²

The one condition is that you genuinely become a Dubai resident. That is where Meydan Free Zone comes in, setting up the company and residency that make the move real.

Assurance-Vie and PEA After Leaving France

The assurance-vie is an investment account that grows over time and is taxed lightly the longer you hold it. The PEA is simpler: an account for investing in shares, with the gains taxed very lightly once you have held it a few years.

The good news is that neither has to close when you move to Dubai. What changes is only how they are taxed once you are a non-resident:

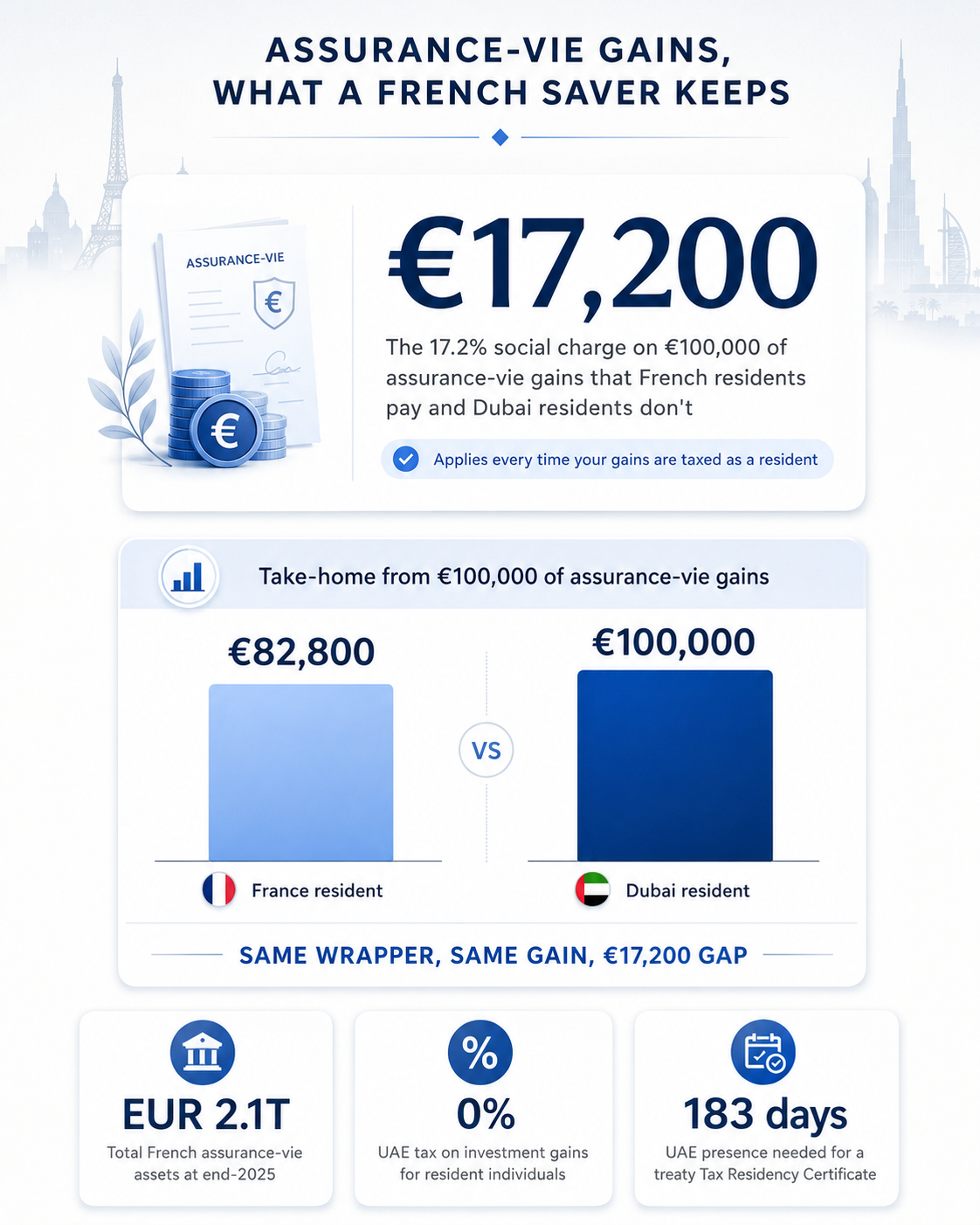

On the assurance-vie, that dropped charge is the standout saving: on €100,000 of gains, the 17.2% you would pay as a resident is €17,200 kept in your pocket.

Two rules sit behind all of this:

- You keep what you have, but you cannot open a new PEA once you have left France, so set it up before you go if you want one.

- The benefits only apply if your move is genuine, France has to actually treat you as a non-resident, which means really living in Dubai, not just holding a visa.

Every one of these benefits rests on being a genuine, provable Dubai resident. And the cleanest way to build that is through a Dubai business setup, the company and visa that make your move real.

Source: France Assureurs January 2026 Communiqué, PwC UAE Individual Taxes 2026, and French Public Finances Directorate (DGFiP), via France Assureurs

What to Review Before Leaving France

Before leaving France, look at what you already have, how old each product is, and whether you may need cash soon after the move.

- PEA age: If your PEA is already over five years old, it is usually more flexible and may be worth keeping.

- PEA withdrawals: Taking money out too early can close the plan, so do not withdraw casually before checking the rules.

- Assurance-vie age: Contracts over eight years usually get better tax treatment, making timing important.

- Unrealised gains: If the account has grown significantly, large withdrawals should be planned carefully.

- Beneficiary clause: Moving to Dubai may change your wider succession plan, so the beneficiary clause should be reviewed.

- Bank or insurer policy: Some providers may ask for your new address, tax residence, Emirates ID, UAE visa or other non-resident documents.

[blockCTAmResidency]

Why Dubai Is a Tax-Light Base for French Investments

Your Assurance-Vie and PEA may survive the move, but the country you move to decides whether another tax layer appears.

Many countries tax worldwide investment income, dividends, interest or realised gains, which can reduce the benefit of keeping French wrappers abroad. Dubai does not add that extra layer.

So a French saver in Dubai gets the best of both worlds: France steps back, no 17.2% charge on the assurance-vie, and Dubai adds 0% on top. Your money stays invested and growing in a genuinely tax-light home.

Building Your UAE Residency File With Meydan Free Zone

Once you leave France, your bank, broker or insurer may ask a simple question: where are you tax resident now?

That matters because your assurance-vie and PEA stay French, but your status changes. To update that status properly, you need more than a Dubai address. You need a documented UAE base: company, visa, Emirates ID, banking, accounting records and, once eligible, Tax Residency Certificate documents.

The TRC is the key document, and the UAE grants it on real presence. You qualify as a UAE tax resident through any one of these:

- 183+ days in the UAE over a 12-month period, the standard route

- 90+ days, if you also hold a UAE residence permit and a home or business here

- Centre of interests, your main home and financial life are based in the UAE

That is where Meydan Free Zone fits in. Meydan Free Zone does not manage your assurance-vie or PEA; but builds the UAE side that supports the move:

- Set up your company: A 100% owned Free Zone LLC (FZ LLC), licensed online, with Fawri available in under 60 minutes.

- Get your residency: mResidency supports the investor visa, medicals, biometrics and Emirates ID processes end-to-end, giving you the documents that show you are legally based in Dubai.

- Build your banking trail: Corporate banking and guaranteed IBAN support through partner banks helps your income and business activity move through UAE accounts.

- Keep your records clean: mPlus supports accounting, corporate tax, UBO compliance and company documents, and helps prepare your Tax Residency Certificate once you qualify, which rests on real presence in the UAE, at generally 183 days a year.

Pricing is straightforward: the regular license starts from €2,971 (AED 12,500), or €3,566 (AED 15,000) if you want the instant Fawri setup.

Together, these documents show the bigger picture your bank, insurer or adviser needs to see: where you live, where your business runs, where your income flows, and whether your Dubai move is properly documented.

That is the real role of Meydan Free Zone here: building the Dubai base that lets those French products be reviewed from a genuine non-resident position.

In Conclusion

Moving to Dubai does not cost you your assurance-vie or your PEA. In most cases you keep both. As a genuine non-resident, France taxes them more lightly, the 17.2% social charge on the assurance-vie falls away, and PEA withdrawals sit outside French tax, while Dubai adds nothing on top.

The catch is the word "genuine." These benefits follow a real move, not a visa left in a drawer. So the smart order is simple: keep the products, build a documented Dubai base, and get your residency right before touching anything.

That is the part Meydan Free Zone handles, the company, residency and records that prove your move is real. If you are planning it, book a free consultation with a setup advisor at Meydan Free Zone.

[blockCTAContact]

Footnotes

¹ France Assureurs, Communiqué, Janvier 2026, assurance-vie assets reached €2,107 billion at end-December 2025, 2026.

² PwC, United Arab Emirates: Taxes on Personal Income, no UAE personal income tax or capital gains tax for individuals, 2026.