Table of Contents

Frequently Asked Questions

1. Is healthcare free in Dubai for UK expats like the NHS?

No, healthcare in Dubai is not free for UK expats. Unlike the UK's NHS, which is funded by taxation, Dubai's system is based on mandatory private health insurance. All residents, including expats, are legally required to have medical coverage, which is typically provided by their employer or purchased privately [1].

2. How does mandatory health insurance work for expats in Dubai?

Employers in Dubai are legally required to provide a minimum level of health insurance for their employees. However, this basic coverage may not be sufficient for all needs. Many expats choose to upgrade their plan or purchase separate policies for dependents to gain access to a wider network of private hospitals and specialists.

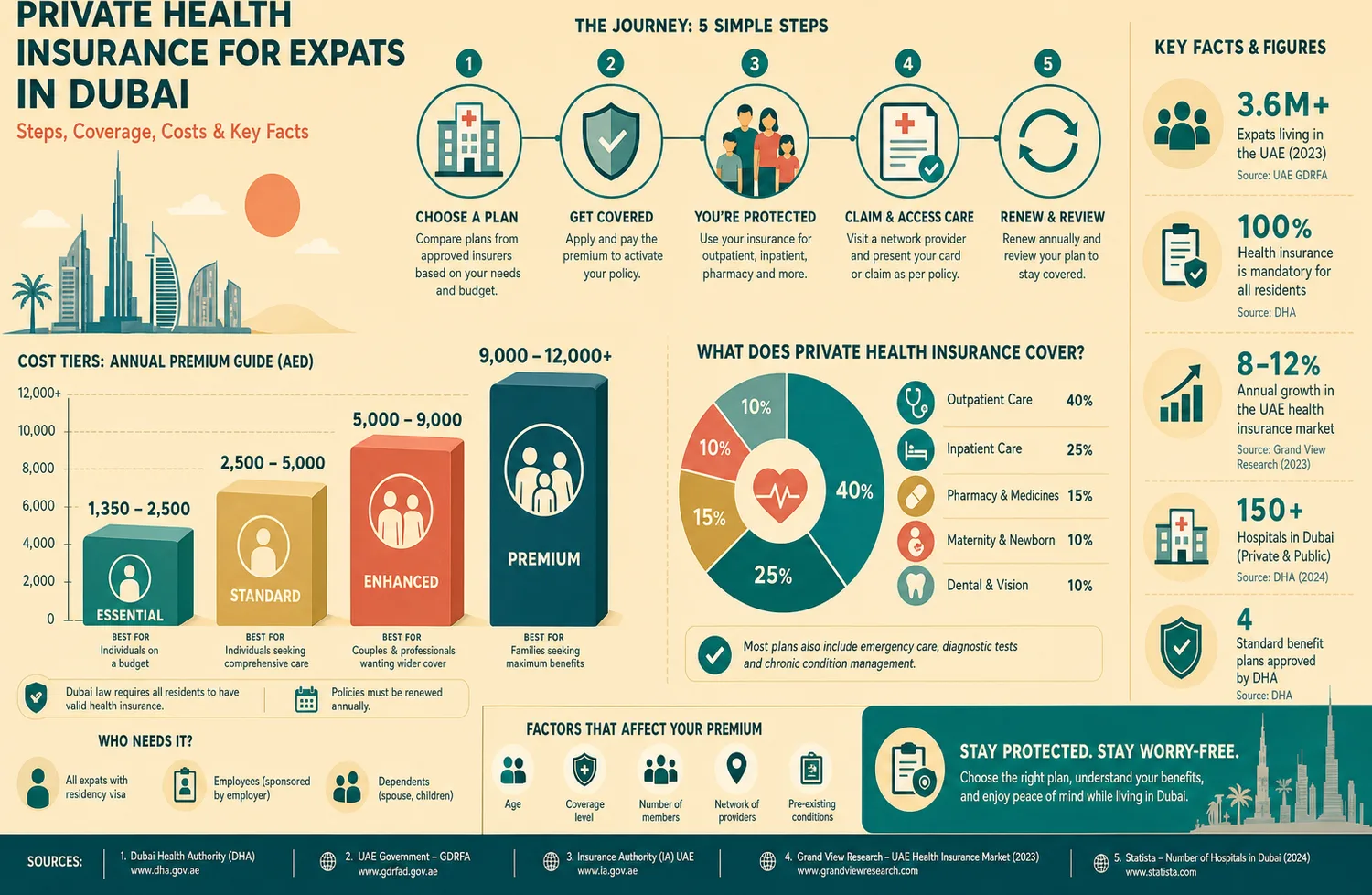

3. What are the average costs for expat health insurance in Dubai?

Costs vary significantly based on age, coverage level, and provider network. Basic plans can start from AED 600 annually, while comprehensive plans with extensive benefits can exceed AED 15,000 per year.

4. How do I choose the right private medical care in Dubai?

Start by checking which hospitals and clinics are included in your insurance plan's network to avoid out-of-pocket costs. Research hospital reputations, specialist availability, and patient reviews. It's wise to confirm if they offer direct billing with your insurer to simplify the payment process.

5. What documents are needed to get health insurance in Dubai?

To set up health insurance in Dubai, you will first need a valid UAE residence visa, along with copies of your passport, visa, and Emirates ID. Start by reviewing any coverage provided by your employer, then identify your healthcare priorities, such as maternity, dental, or preferred hospitals. After that, compare insurance plans based on coverage, network, and overall cost before completing the application process and receiving your insurance card.

Topic Summary

1. Mandatory Insurance Is Your Visa Key

In Dubai, securing a residency visa is directly tied to having valid health insurance. Employers must provide coverage for their employees, but you are legally responsible for insuring any dependents, like a spouse or children (1).

2. Assess Your Employer's Plan Carefully

The basic plan offered by your employer might have limitations. Check the network of hospitals, coverage limits for specific treatments, and co-pay amounts to decide if you need to upgrade or purchase a separate, more comprehensive plan.

3. Compare Total Cost, Not Just Premiums

A low monthly premium can be misleading. High deductibles and co-payments can lead to significant out-of-pocket expenses. Review the full schedule of benefits to understand your true annual cost.

4. Insurance Tier Comparison at a Glance

Plans vary widely in cost and coverage. Basic plans meet visa requirements, while comprehensive options offer access to premium facilities with lower out-of-pocket costs.

5. Verify Your Preferred Hospitals Are In-Network

Private medical care in Dubai is excellent but only accessible if it's within your insurer's network. Before signing up, confirm that your preferred clinics and hospitals are included to ensure direct billing and avoid paying fully out-of-pocket.

Healthcare in Dubai for UK Expats: Costs & Insurance

If you're researching healthcare in Dubai for UK expats, here's the short answer: you’ll usually rely on private health insurance, either through your employer or a personal policy, and your access, speed, and out-of-pocket costs will depend heavily on your insurer network and plan design. This guide is for UK nationals and families planning a move, and it will help you compare coverage, estimate costs, and choose private care with fewer surprises.

Dubai’s system is closely regulated by the Dubai Health Authority, while insurance rules are shaped by local mandatory coverage requirements for residents. The UAE ranked 20th globally in the Legatum Health Pillar in 2023, and Dubai continues to attract international hospital operators and specialist groups, which is why many expats see it as a strong private-care market rather than a public-health destination (Legatum Institute, 2023).

How Does Healthcare in Dubai for UK Expats Work

Definition and Core System Structure

Healthcare in Dubai for UK expats is built around insured access to private clinics, day-surgery centers, and hospitals. Public facilities exist, but most expats use private providers for routine GP visits, pediatrics, diagnostics, maternity, and specialist care.

The legal framework matters. Dubai’s health insurance system has been shaped by Insurance System of Advancing Healthcare in Dubai, Law No. 11 of 2013, which established mandatory health insurance requirements in the emirate (Dubai Health Authority, 2013).

Who Pays and How Access Is Managed

In practice, your employer often pays for your base plan, but family coverage may be partly or fully your responsibility. If you’re self-employed, retired, or relocating without an employment package, you’ll need to buy an approved policy yourself.

Access is managed through insurer networks, pre-authorization rules, annual limits, co-pays, and exclusions. A cheaper premium can still leave you with higher bills if your preferred hospital group sits outside network.

What You Should See at This Stage

You should now see the big picture: Dubai offers fast, private-led care, but policy wording matters almost as much as provider quality. That’s the core of healthcare in Dubai for UK expats.

Prerequisites Before You Compare Insurance and Care Options

Tools and Documents

Before you compare plans, collect the basics: passport copy, visa or entry status, Emirates ID stage if available, employer benefits summary, and dependent details. Add current prescriptions, chronic conditions, expected maternity needs, and your preferred clinics or hospital groups.

Knowledge and Time Needed

You’ll also want a realistic budget. Don’t look only at annual premium numbers, look at co-pays for consultations, pharmacy limits, outpatient caps, dental add-ons, and whether chronic conditions are covered after a waiting period.

If you’re moving from the NHS mindset, this shift is important. In Dubai, convenience is often excellent, but it’s structured through insurer approval and direct billing rules rather than universal no-cost access.

What You Should See at This Stage

At this point, you should have a shortlist of needs, not just a vague request for “good insurance.” That makes broker quotes far more useful and easier to compare side by side.

5 Steps to Set Up Coverage and Private Medical Care

1. Define Your Care Priorities

Start with your real use case. Are you a single professional who needs quick GP access, or a family that needs pediatrics, maternity, and asthma medication refills?

2. Verify Mandatory Coverage Arrangements

Check whether your employer already enrolled you and when coverage starts. Gaps can happen between arrival, visa processing, and policy activation, so confirm effective dates in writing.

3. Compare Total Cost, Not Just Premium

Ask for the schedule of benefits. You need to see deductibles, co-insurance, outpatient limits, maternity waiting periods, annual maximums, and whether tests like MRI or CT scans need prior approval.

4. Shortlist Providers and Test Access

Then test the network in real life. Search for nearby primary care clinics, call two hospitals, and ask about appointment wait times, direct billing, and specialist availability in the insurer portal.

5. Confirm Claims Rules Before Your First Visit

This step is often missed. Make sure you know when you can use direct billing, when you pay first and claim later, and which services need pre-authorization, especially maternity, surgery, and advanced imaging.

Costs, Table, and Budget Benchmarks

Main Cost Drivers to Review

Costs in Dubai vary by age, underwriting, hospital network, and benefits. Premiums for a healthy single adult can be far lower than for a family with children, ongoing prescriptions, or planned maternity care.

Provider pricing also changes the math. A specialist visit at a premium private hospital will usually cost much more than a network clinic, even if both are covered partly under your plan.

| Cost Item | Typical Dubai Range | What to Check |

|---|---|---|

| GP consultation | AED 150 to AED 400 | Clinic tier, direct billing, co-pay |

| Specialist consultation | AED 300 to AED 700 | Referral rules, network status |

| Basic individual annual plan | AED 5,000 to AED 12,000+ | Annual limit, exclusions, network |

| Maternity-inclusive plan | Often materially higher than base plans | Waiting period, delivery caps, newborn cover |

| Emergency treatment | Can run into several thousand AED | Hospital category, deductible, approvals |

What You Should See at This Stage

You should now be budgeting for total annual spending, not just the premium. For healthcare in Dubai for UK expats, weak-value plans usually reveal themselves through narrow networks and high out-of-pocket bills.

Private Medical Care Options and Quality Checks

How to Assess Clinics and Hospitals

Start with licensing and inspection credibility. Dubai Health Authority regulates healthcare facilities and professionals in the emirate, so check whether the provider is properly listed and active before you commit (Dubai Health Authority, 2024).

Then look at practical quality markers: specialist depth, imaging on site, pharmacy hours, direct billing, and whether follow-up care is coordinated well. Fancy interiors don’t tell you much. Operational consistency does.

Specialist Access and Continuity of Care

If you need endocrinology, dermatology, pediatrics, or women’s health, confirm appointment lead times before choosing a plan. Some insurers include excellent hospitals on paper, but available slots can still be limited in popular branches.

Red Flags to Screen Out

Watch for vague benefit summaries, poor broker explanations, and plans that exclude the providers you actually want to use. Also be careful with policies that offer low premiums but high co-insurance on diagnostics and specialist visits.

Success Criteria and Next Steps

You’re ready when you can answer five questions clearly: Who is paying for the policy, which hospitals are in network, what your likely annual out-of-pocket spend looks like, which services need approval, and where you’ll go for your first routine appointment. If any of those answers are fuzzy, don’t buy yet.

The smartest next step is simple: request two like-for-like quotes, compare the network list line by line, and call your top clinic before enrollment. That’s how healthcare in Dubai for UK expats becomes a practical plan instead of a guess.

Citations

- Dubai Health Authority, 2013, Insurance System of Advancing Healthcare in Dubai Law No. 11 of 2013: https://www.dha.gov.ae

- Dubai Health Authority, 2024, official healthcare regulation and provider information: https://www.dha.gov.ae

- UAE Government Portal, 2024, health and insurance information: https://u.ae

- Legatum Institute, 2023, Prosperity Index Health Pillar: https://www.prosperity.com