Table of Contents

Frequently Asked Questions

1. Can a British accounting firm set up in Dubai through a free zone?

Yes. British accounting firms can establish a presence in Dubai through a free zone entity, which allows 100% foreign ownership and the ability to provide accounting, bookkeeping, and tax advisory services to UAE and international clients.

2. What business activities should a British accounting firm choose in Dubai?

The most relevant activities include Accounting, Bookkeeping and Auditing Activities; Tax Consultancy, along with Accounting & Bookkeeping and Preparation or Auditing of Financial Accounts, depending on the firm’s service scope.

3. Why is there strong demand for accounting services in Dubai?

Demand is driven by regulatory changes. The introduction of corporate tax, mandatory audits for QFZPs, VAT compliance, and transfer pricing requirements has created ongoing demand for professional accounting services.

4. What types of clients do accounting firms typically serve in Dubai?

Clients include free zone companies, mainland businesses, and international firms operating in the UAE. Many require ongoing bookkeeping, VAT filings, corporate tax support, and audit-ready financial reporting.

5. How long does it take to set up an accounting firm in Meydan Free Zone?

A standard business license can be issued within one working day once documents are approved. For simpler setups, faster incorporation options are also available.

Topic Summary

1. Compliance Area Requirements

In the UK, compliance is mandatory for most limited companies with exemptions available for small companies. Conversely, in the UAE, compliance is mandatory for all Qualifying Free Zone Persons (QFZPs) and companies with revenues exceeding AED 50 million, with enforcement primarily conducted through corporate tax filings.

2. Accounting Standards Applied

UK entities generally apply either UK Generally Accepted Accounting Practice (UK GAAP) or International Financial Reporting Standards (IFRS). In contrast, UAE companies use IFRS or IFRS for Small and Medium-sized Entities (IFRS for SMEs), with no separate local Generally Accepted Accounting Principles (GAAP).

3. Corporate Taxation Framework

The UK imposes a corporate tax rate of 25% on profits exceeding £250,000. The UAE, however, implements a 0% rate on qualifying free zone income and levies a 9% corporate tax on profits above AED 375,000.

4. Value Added Tax (VAT) Rates

The UK applies a standard VAT rate of 20%, whereas the UAE’s standard VAT rate stands at 5%. Additionally, the UAE distinguishes more clearly between zero-rated and exempt categories of goods and services.

5. Audit Requirements

Audit mandates in the UK typically apply to most limited companies, with specific thresholds that exempt smaller entities. In the UAE, audit requirements align closely with the corporate tax law thresholds and free zone regulations, often necessitating audits for entities exceeding set financial criteria.

Setting Up British Accounting and Audit Services for Dubai Companies

British accounting practices are not short of qualified people. What they are running short of is margin. Per the Law Society's most recent financial benchmarking survey via Global Legal Post¹, underlying UK profit performance flatlined at 1.2% in 2024 once client interest is stripped out, and accountancy firms are navigating the same pressures: rising staff costs, fixed-fee demand from clients, and the Big Four absorbing the higher-value advisory work that mid-tier firms used to own.

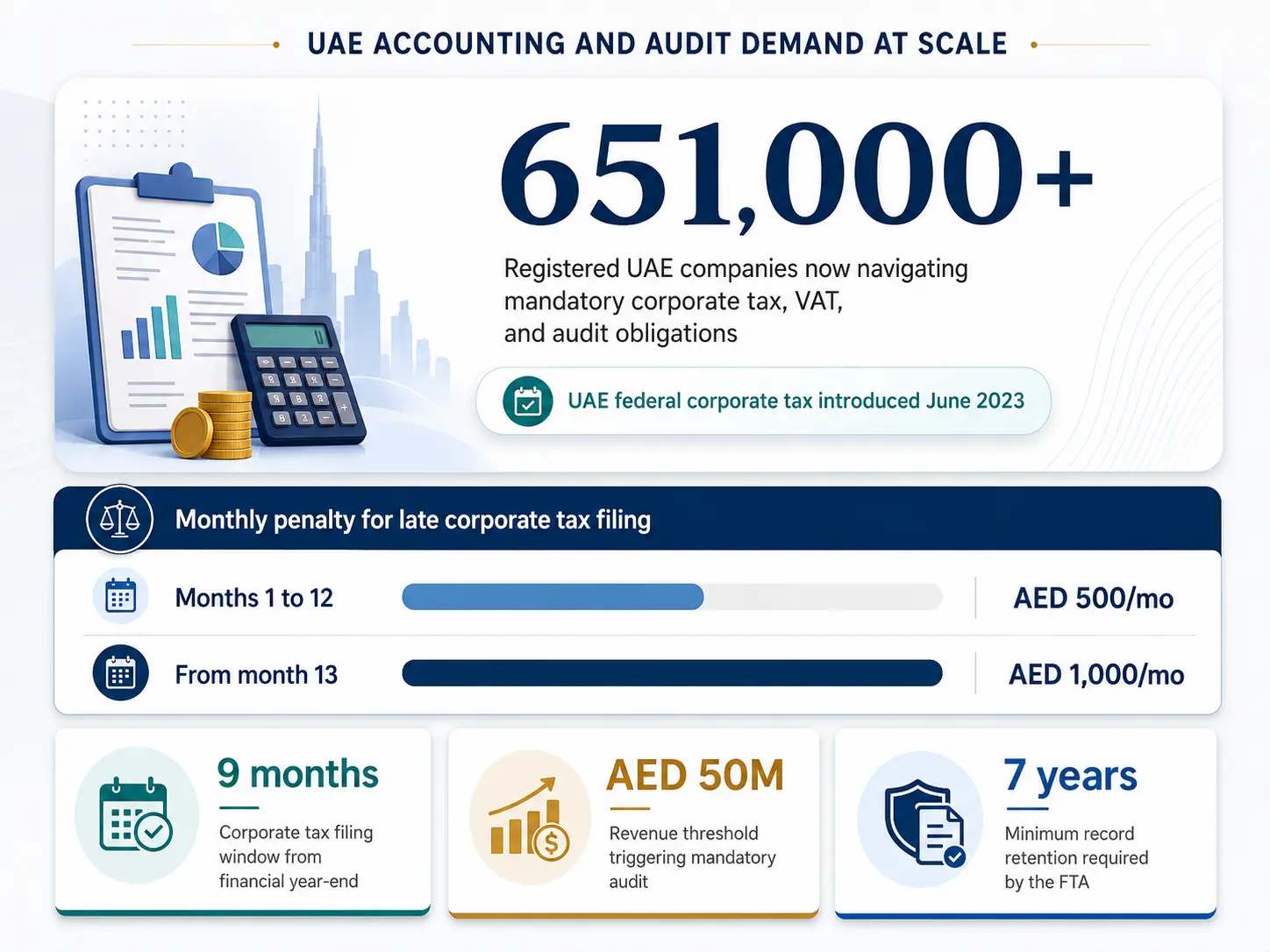

Dubai's compliance landscape, meanwhile, is heading in the opposite direction. Setting up British accounting services in Dubai is becoming a commercially serious conversation precisely because the UAE has spent the last two years creating layers of mandatory compliance that most of its 651,000+ registered companies are underprepared to handle. ACCA and ACA qualifications are directly applicable in the UAE, IFRS is the required standard, and British-trained practitioners understand both frameworks natively.

Here is what the demand looks like, what the compliance picture requires, and how a British accounting practice actually operates within it.

[blockCTACostCalculator]

Why Dubai's Audit and Accounting Demand Is Structural

The driver here is straightforward. The UAE introduced federal corporate tax in June 2023. For most of the business community, this was the first formal tax obligation they had ever operated under. The compliance requirements that come with it are not minor.

Under Ministerial Decision No. 84 of 2025, two categories of UAE businesses must now maintain audited financial statements as a legal obligation:

- All Qualifying Free Zone Persons (QFZPs), regardless of revenue size

- All taxable persons with annual revenue exceeding AED 50 million

This is where the structure becomes commercially important.

Meydan Free Zone is a Qualifying Free Zone, which means businesses set up within it can access the 0% corporate tax rate on qualifying income. But that benefit is conditional. For QFZPs, audited IFRS-compliant financial statements are not just a reporting requirement, they are a statutory requirement to retain that 0% status.

A QFZP that fails to maintain audited accounts does not simply fall out of compliance. It loses its preferential tax treatment and is taxed at 9% on all income, not just non-qualifying income. The financial impact of that shift is material, particularly for businesses operating at scale or across borders.

Beyond audit, the compliance layer continues to expand. UAE companies must now manage VAT filings, maintain transfer pricing documentation for related-party transactions above defined thresholds, and submit corporate tax returns within nine months of the financial year-end.

For companies with a December year-end, that deadline falls on 30 September. Missing it triggers penalties starting at AED 500 per month, increasing to AED 1,000 from the thirteenth month. Financial records must be retained for a minimum of seven years.

Two years ago, most businesses in the UAE were not operating under any of these requirements. Today, they are expected to maintain audit-ready, IFRS-aligned financial systems as standard.

[blockCTANameCheck]

The Compliance Market in Numbers

UAE compliance went from optional to mandatory in 2023, and the entire registered business base is still catching up. Here is the scale of the addressable market and the cost of falling behind.

Source: UAE Federal Tax Authority, Ministerial Decision No. 84 of 2025, and PwC Middle East Tax News Alerts, via UAE Federal Tax Authority

What Dubai Companies Actually Need

The compliance stack for a typical UAE company in 2025 breaks down into four practical service areas:

[blockFaqsCategory]

[blockCTABizActivityList]

The Structural Comparison

The technical overlap is high. British-trained accountants already work to IFRS and understand audit under ISA principles. The UAE does not have its own accounting standards. IFRS is the framework. For a UK-qualified accountant, the learning curve is regulatory context and not accounting methodology.

For context, UK corporation tax sits at 25% for companies above £250,000 in profit. The UAE's 0% QFZP rate is a structurally different starting point for the same conversation. Read more about UAE corporation tax rates.

[blockCTATradeLicense]

What a British Accounting Practice Needs to Operate in Dubai

The right structure for a British accounting practice in Dubai depends on the services it intends to deliver. In practice, most firms entering the market do not begin with audit. They start with advisory, compliance, and reporting, which is where the immediate demand sits.

In Meydan Free Zone, this model is supported through professional activities including:

- Accounting, Bookkeeping and Auditing Activities; Tax Consultancy: Broad-scope category covering day-to-day financial management, VAT support, and corporate tax advisory.

- Accounting and Bookkeeping: Focused on ongoing transactional record-keeping and management reporting.

- Preparation or Auditing of Financial Accounts: Covers financial statement preparation aligned with IFRS standards.

- Examination and Certification of Accounts: For firms providing specialised certification work for compliance purposes.

These activities form the operational backbone for firms providing the services most businesses now require under the UAE's tax regime. This structure allows British firms to:

- Operate as a fully foreign-owned UAE entity with 100% ownership retained

- Contract directly with clients in AED on local payment terms

- Deliver ongoing compliance, reporting, and advisory that aligns with how accounting work is actually consumed in the UAE market

[blockCTAFawri]

Where Meydan Free Zone Fits In

Meydan Free Zone is a Qualifying Free Zone, which makes it structurally relevant for accounting and audit practices.

Businesses operating within the free zone can qualify for the 0% corporate tax rate on qualifying income, provided they meet the conditions of a Qualifying Free Zone Person (QFZP). One of those conditions is maintaining audited financial statements. It creates a continuous, recurring demand for accounting, bookkeeping, and audit-ready financial reporting across the entire client base operating within the free zone.

For accounting firms, this matters in two ways.

First, it ensures a steady pipeline of compliance-driven work. Every QFZP must maintain proper books, prepare IFRS-aligned financial statements, and remain audit-ready to retain its tax status.

Second, it aligns the firm directly with the regulatory structure of the market it is serving. The accounting practice is not operating in isolation; it is embedded within a system where compliance is tied directly to tax outcomes.

Combined with a fully digital setup process, 100% foreign ownership, and the ability to issue a business license within one working day once documents are approved, Meydan Free Zone provides a practical entry point for firms looking to establish an accounting presence in Dubai without unnecessary structural complexity.

[blockCTABizSetupRemotely]

In Conclusion

The case to setup British accounting services Dubai is driven by regulatory demand, not promotional optimism. More than 651,000 UAE companies are navigating mandatory audit obligations, corporate tax filings, transfer pricing documentation, and VAT compliance. Many are doing it without the qualified professional infrastructure to do it properly. British-trained accountants understand IFRS, work to ISA audit standards, and bring the methodological frameworks this market now legally requires.

Meydan Free Zone's mAccounting covers the practice's own UAE compliance from day one: bookkeeping, VAT registration, corporate tax filings, and financial audit reports. That is one less operational distraction while building the client base.

Ready to get started? Use the Meydan Free Zone cost calculator to plan your setup.

Footnotes

¹ Law Society of England and Wales, via Global Legal Post, "Mid-Market UK Firms Grew Turnover by 6% in 2024 Amid Rising Costs," 2025.