Table of Contents

Frequently Asked Questions

1. Is health insurance mandatory for Indian expats in Dubai, and what happens if coverage lapses?

Yes, the Dubai Health Authority mandates active, licensed health insurance for every resident from the date of visa stamping. No exceptions. If coverage lapses, the founder faces residency non-compliance and personal liability for all treatment costs during the gap, there is no grace period extension under DHA rules.

2. Does my employer's Dubai health insurance plan automatically cover my spouse and children?

Most expats discover too late that it does not. Employers are legally required to cover directly sponsored staff only. Spouses and children on dependent visas must select a separate family plan independently, typically costing AED 8,000–14,000 annually. Log into the DHA portal to verify what the employer plan actually covers.

3. What is the DHA EssentialBP plan and is it sufficient for an Indian family with children?

The EssentialBP is the minimum DHA-mandated standard,covering emergency care and inpatient treatment up to AED 150,000. For a family with children, it is often insufficient: it excludes dental, optical, and maternity, and the inpatient limit can run from below what a single surgical admission costs at a private Dubai hospital.

4. Are pre-existing conditions like diabetes or hypertension covered under Dubai health insurance plans?

Chronic conditions are often excluded from standard plans or subject to a 12-month waiting period, insurers will reject claims if these were not declared at enrollment. Specify pre-existing conditions accurately when submitting of the following documents to avoid a rejected claim and personal liability.

5. What does health insurance in Dubai cost annually for an Indian family of four?

A family of four should budget approximately AED 14,000–20,000 annually for a mid-to-comprehensive plan covering all members with a maternity add-on. The founder must select a DHA-Licensed Plan and verify the network includes their preferred provider, Aster, Mediclinic, or NMC, before enrolling.

Topic Summary

1. DHA Mandates Coverage From Visa Stamping

The Dubai Health Authority requires active, licensed health insurance from the date of visa stamping, there is no grace period extension. Indian expats who assume coverage starts later face personal liability for any treatment costs during the gap.

2. Employer Plans Often Exclude Dependents

What most Indian expats discover too late: corporate plans cover the employee only. Spouses and children on dependent visas must select a separate licensed plan, often costing AED 8,000–14,000 annually, or remain uninsured.

3. Chronic Conditions Require Declaration at Enrollment

Conditions like diabetes, hypertension, and thyroid disorders are often excluded from standard plans, insurers will reject claims if these were undeclared. Failing to disclose pre-existing conditions at enrollment creates direct financial consequences.

4. Verify Active Status on the DHA Portal

An HR confirmation email does not equal live DHA-registered coverage. Log into the DHA portal to confirm the policy is active against each Emirates ID before the first clinic visit, this is the only verification that counts.

5. Maternity and Repatriation Gaps Create Serious Exposure

Maternity coverage typically carries a 12-month waiting period, and repatriation of remains to India is not covered under standard DHA plans. Families who discover too late face costs of AED 15,000–35,000 for delivery alone.

6. Budget for the Full Family, Not Just the Employee

A family of four should budget approximately AED 14,000–20,000 annually for mid-to-comprehensive coverage. Factor in recurring fees for renewal, and select a plan with explicit add-on coverage for dental, optical, and pediatric care.

Healthcare and Medical Insurance in Dubai for Indian Expats and Families

Healthcare in Dubai for Indian expats runs on a mandatory private insurance model, there is no public entitlement for expat Residents. No exceptions. The Dubai Health Authority (DHA) accredits providers, sets minimum benefit standards, and mandates active, licensed coverage from the date of visa stamping, not from Emirates ID issuance.

Before the founder selects any plan, four of the following must be in hand: a valid UAE residence visa for each family member, Emirates ID in process or being compiled, clear colour copies of all passports with at least six months' validity, and an employer letter or Trade License confirming Sponsorship. Government portals all request these at multiple stages.

An Indian IT professional relocating to Dubai Business Bay with a spouse and two children needs four separate enrollment records, one per family member, before any clinic visit is covered. Allow two to four weeks from visa stamping to active insurance card in hand; the process is not same-day.

How the Dubai Healthcare Model Works

The DHA accredits providers, sets the EssentialBP minimum standard, and maintains the licensed insurer list, only DHA-approved plans satisfy the residency requirement. Mandatory coverage applies from the date of visa stamping, there is no grace period extension under DHA rules. Employers Sponsoring staff must maintain health insurance as a mandatory condition; failure creates direct liability for the sponsor.

Healthcare Model Does Not mirror India's system. Dubai's model is built on private insurance, it does not function like AIIMS or state hospitals. Government hospitals like Rashid Hospital and Dubai Hospital operate on an insurance-first model for expat Residents, they do not provide free or low-cost treatment to uninsured Residents. Out-of-pocket costs without insurance can run from AED 300 for a GP visit to AED 15,000 or more for a single clinic visit to confirm coverage is opened and functional.

Coverage Responsibility: Who Pays for Whom

Coverage Responsibility follows the visa Sponsorship chain. Employers cover directly sponsored staff, but that obligation does not extend to the employee's dependents unless the contract specifies it. Many corporate plans cover the employee only; spouses and children on dependent visas require a separate family plan. An Indian engineer at a Dubai tech firm often discovers their corporate plan covers only the employee; their spouse and two children require a separate plan costing AED 8,000–14,000 annually.

Self-sponsored founders, covering ownership through their own company, bear full Coverage Responsibility for themselves and any dependents on their visa. Direct sponsorship means the founder maintains full coverage responsibility. Budget approximately AED 5,000–9,000 annually for self-coverage and AED 12,000–22,000 for a family of four, depending on plan tier and age of dependents. Chronic conditions are often excluded from standard plans, declare pre-existing conditions accurately at enrollment to avoid claim rejection.

Plan Tier Comparison

| Plan Tier | Annual Cost (AED) | Covers | Best For |

|---|---|---|---|

| Essential (EBP) | 650–1,000 | Emergency, inpatient up to AED 150,000, basic outpatient | Single low-risk employee only |

| Mid-Tier | 3,000–8,000 | Extended inpatient, specialist access, one dependent | Young families without chronic conditions |

| Comprehensive | 8,000–25,000 | Maternity, dental, optical, mental health, higher inpatient | Families with chronic conditions or planned maternity |

What Most Indian Expats Discover Too Late

Chronic conditions - diabetes, hypertension, thyroid disorders - are subject to a six-month waiting period under DHA-regulated plans, during which only emergency care related to these conditions is covered. Some higher-tier private plans extend this further. Critically, non-disclosure of any pre-existing condition at enrollment can result in claim refusal or outright cancellation of the policy, so declare everything accurately. Optical care is not included in the EssentialBP baseline and requires an explicit add-on - verify what is and is not covered before signing. An Indian family with a diabetic parent who fails to declare the condition at enrollment can find a hospitalisation in month three results in a fully rejected claim and personal liability running into tens of thousands of dirhams. ¹

Maternity coverage requires equal care. Under EBP, any pregnancy conceived within 40 days of the policy start date is not covered unless agreed and paid for as an additional premium, and higher-tier private plans commonly impose waiting periods of 6 to 12 months. A couple arriving in Dubai three months before a planned pregnancy can find themselves paying AED 12,000 to 24,000 or more out of pocket for delivery at a private hospital. Repatriation of remains to India is not covered under standard DHA plans - a cost most expats discover too late falls entirely on the family. And when employment ends, employer-provided coverage typically cancels with the visa, though some insurers extend a 30-day grace period limited to emergency care only - planned treatment must either be completed beforehand or covered by a new private policy to avoid both medical bills and legal exposure during the transition. ²

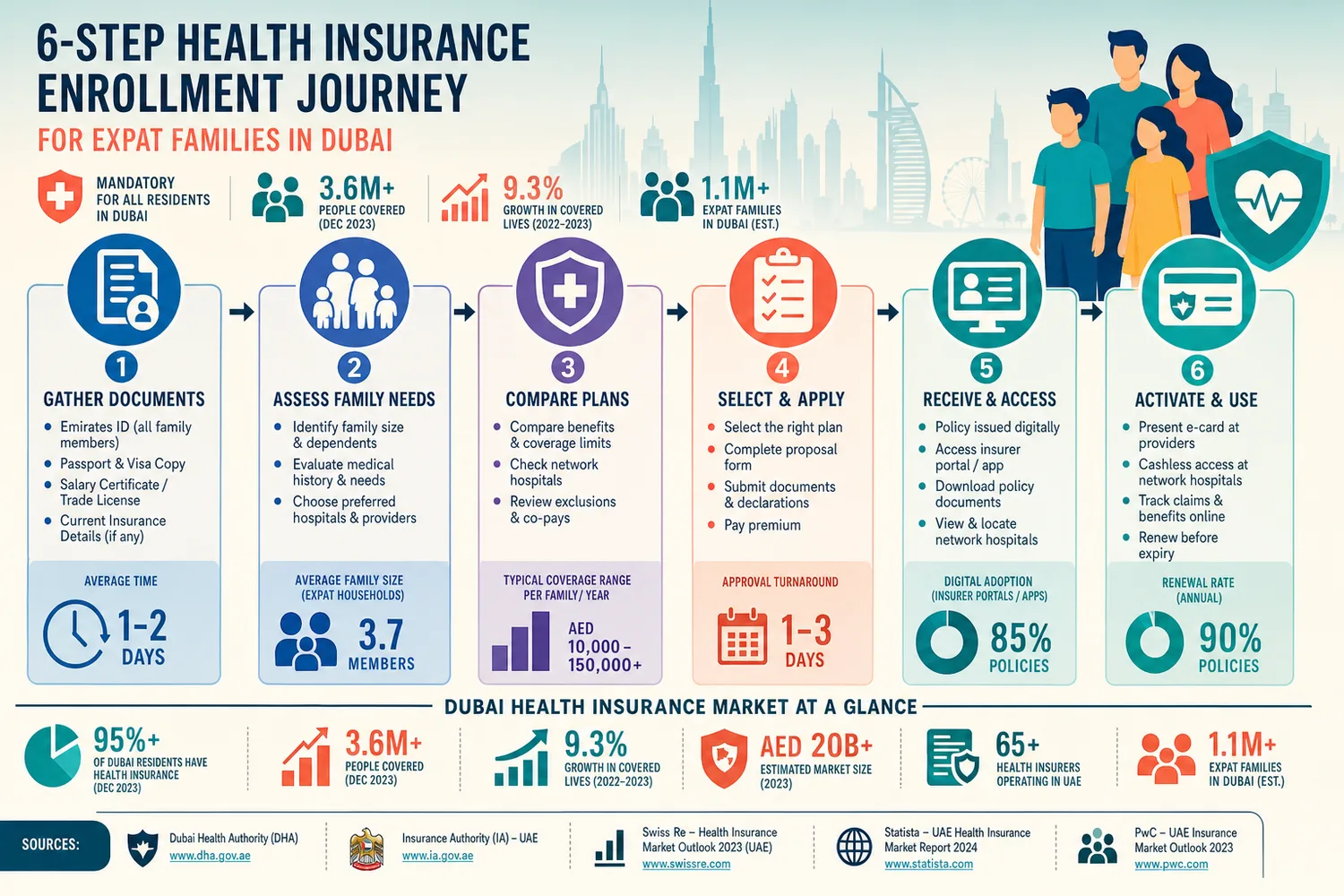

A Numbered Process: How to Get Covered

Getting health insurance in Dubai follows a defined sequence: confirm visa sponsorship, define coverage scope, select a licensed plan, submit documents, verify active status, and collect your insurance card. Each step opens the next - skipping any one of them stalls the entire process.

Step 1 - Confirm visa sponsorship. Determine who is sponsoring each family member: the employer, your own company (for self-sponsored founders), or a family member. The sponsor carries the coverage responsibility and drives the rest of the paperwork.

Step 2 - Define coverage scope. Catalogue each family member individually - name, age, and any pre-existing conditions such as diabetes, hypertension, or thyroid disorders. Declare these accurately. Undisclosed conditions are the single most common reason claims are rejected later.

Step 3 - Select a licensed plan. Choose only from DHA-approved insurers, and confirm the plan's network includes the providers you actually want to use - Aster, Mediclinic, NMC, or others near your home and workplace. Match the tier (EssentialBP, Mid-Tier, or Comprehensive) to your family's real needs rather than the lowest sticker price.

Step 4 - Submit the required documents. Passport copies with at least six months' validity, residence visa copy, Emirates ID application receipt, and the completed enrollment form. Incomplete submissions typically add three or more days to the timeline.

Step 5 - Verify active status. Once the insurer confirms enrollment, log into the DHA portal to confirm the policy is live and linked correctly to each Emirates ID. Do not rely on the insurer's email confirmation alone - verify directly with the regulator.

Step 6 - Collect your insurance card. The physical card is issued within three to five business days. Save the insurer's 24-hour emergency contact number separately in your phone - you will need it before the card arrives.

Conclusion

Securing the right health insurance plan in Dubai takes preparation, not guesswork. Indian expat families who map out each member's coverage needs early - accounting for ages, pre-existing conditions, and dependent visa obligations - avoid the gaps that most expats discover too late: rejected maternity claims, excluded chronic conditions, and uncovered repatriation costs.

The DHA mandate is not optional. The moment residency is stamped inside your passport, coverage responsibility begins - there is no grace period. A licensed plan selected before that date, verified active through the DHA portal, and renewed on schedule is the foundation of compliant, uninterrupted healthcare for your entire family in Dubai. Treat it as a Day One priority rather than a post-arrival task, and the rest of the relocation becomes considerably easier to manage.