Table of Contents

Frequently Asked Questions

1. Can South Africans open a bank account in Dubai without a UAE residence visa?

No. A stamped UAE residence visa is mandatory before any bank will treat the application as valid. Tourist visa status is not sufficient for a resident personal or corporate account, and booking an appointment without it results in a wasted visit.

2. How long does it take to open a corporate bank account in Dubai as a South African?

Standard processing runs five to seven business days once a complete file is submitted. However, the total timeline from Trade License issuance to a functional account can run from six to ten weeks if the Establishment Card isn't opened and functional and the residence visa isn't stamped first.

3. Does South Africa's FATF grey list status affect UAE bank account applications?

Yes. South Africa was placed on the FATF grey list in 2023, and UAE banks applied enhanced due diligence to South African applicants as a result. South Africa's removal was confirmed in 2025, but individual banks may maintain their own internal risk classifications, confirm with the bank before submitting.

4. What documents do UAE banks require from South African corporate account applicants?

UAE banks need a Trade License, Establishment Card, Memorandum of Association, passport copies for all shareholders, projected annual revenue documentation, signed client contracts, and source-of-funds documentation. Having a professional online presence and a real business story is standard.

5. Do South Africans need to exit South African tax residency before opening a UAE bank account?

Formally exiting South African tax residency with SARS isn't a banking prerequisite, but a founder who was not formally tax resident exited before drawing dividends from a UAE corporate account risks being taxed in both jurisdictions. Address South African tax exit obligations before the process starts, not as a parallel task.

Topic Summary

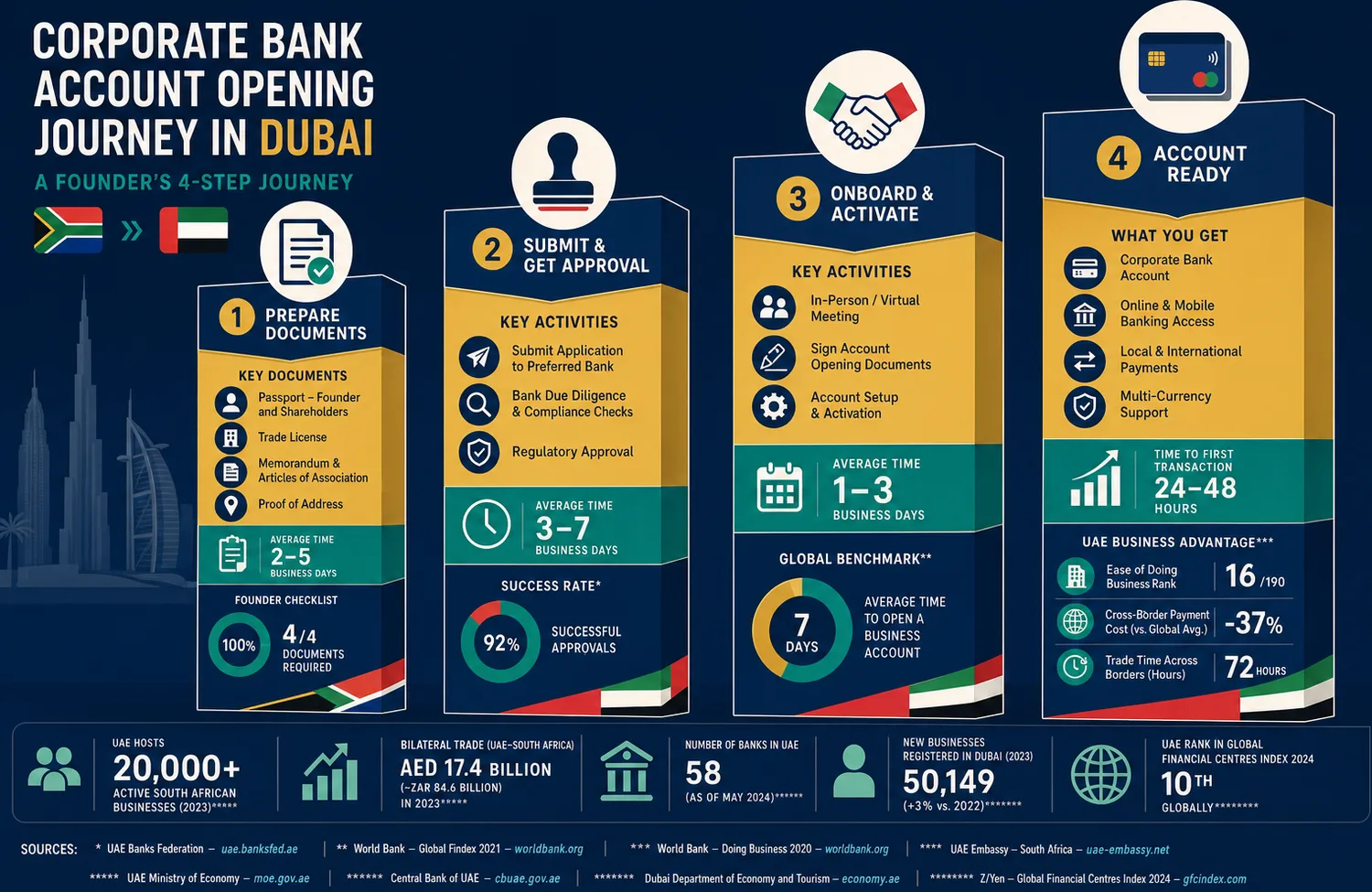

1. The Trade License Comes First

Opening a corporate bank account in Dubai for South Africans isn't automatic after company setup, the Trade License is the foundation, and no corporate process starts without it. The Establishment Card must also be opened and functional before any bank will treat the entity as commercially real.

2. Residence Visa Is Non-Negotiable

UAE banks require a stamped residence visa inside your passport before processing any account. South Africans with only a Trade License faces rejection, the same founder with a stamped visa and documented client contracts rarely gets approval refused.

3. FATF History Adds Compliance Layers

South Africa's FATF grey list status means UAE banks apply enhanced due diligence to South African applicants, adding documentation layers to all corporate account processes. Having a professional online presence, signed contracts, and source-of-funds documentation is standard, incomplete submissions cause delays.

4. Choose the Right Bank Early

Emirates NBD is strongly favoured for corporate accounts and international founders, while ADCB and Mashreq suit digital-first founders with faster onboarding. For personal accounts, Liv by Emirates NBD unlocks setup within one business day once residency is stamped.

5. South African Tax Exit Is Mandatory

South Africans must formally cease tax residency with SARS before the UAE structure delivers any real benefit. A founder who was not formally tax resident exited before opening a UAE corporate account risks being taxed in both jurisdictions, seeking specialist advice before the process starts is not optional.

6. What Most South African Expats Discover Too Late

Booking a bank appointment before the Establishment Card is opened and functional results in a wasted visit. Submitting an incomplete file, missing source-of-funds documentation or projected annual revenue, causes delays of two to four weeks and often requires a restart.

Opening a Corporate and Personal Bank Account in Dubai for South Africans

South African founders arriving in Dubai often assume the bank account follows automatically from the Trade License or residence visa. It doesn't, and that gap between corporate setup and a functional account is where most timelines stall. This guide covers what UAE banks actually need, which institutions to approach, and the compliance realities South Africans specifically face.

What You Need Before You Start

To open a bank account in Dubai as a South African, you need a valid UAE Trade License, a stamped residence visa, an open Establishment Card (Immigration File), and an Emirates ID in process. Corporate accounts also require documented business activity and projected annual revenue.

A South African founder who completes company setup, opens the Immigration File, and gathers corporate documents in week one is positioned to have a functional account within 30 days. Without these prerequisites in place, the bank will not proceed.

What UAE Banks Actually Require from South Africans

For a corporate account, you'll need the Trade License, Establishment Card, Memorandum of Association, Certificate of Incorporation, passport copies for all shareholders, and a business summary covering projected annual revenue and signed client contracts. A founder with only a Trade License and vague business activity rarely gets approval.

South Africa was placed on the FATF grey list in 2023, UAE banks applied enhanced due diligence to South African applicants as a result, adding documentation layers to all corporate account processes. South Africa's removal was confirmed in 2025, but individual banks may maintain their own internal risk classifications. Confirm with the bank before submitting. Having a professional online presence, signed contracts, and a real business story is standard.

A Numbered Process: How to Open a Corporate Bank Account

Follow this sequence precisely. First, confirm the Trade License is issued and the Establishment Card is opened and functional, these are two separate steps. A founder who books a bank appointment before the Establishment Card is issued faces a wasted visit.

Second, gather all corporate documents and build the business narrative: source-of-funds documentation from South Africa, signed contracts, and projected annual revenue. Third, submit everything to your chosen bank and attend the compliance review. The account is not functional until the bank completes its AML and KYC process. The owner who has completed all steps holds a UAE IBAN before the end of week four in most standard cases.

Choosing the Right Bank

Emirates NBD is strongly favored for corporate accounts with minimum balances running AED 25,000–50,000. ADCB suits digital-first founders with faster onboarding and a minimum balance of AED 25,000. Mashreq offers online onboarding with a minimum balance around AED 10,000 for certain setups.

For personal accounts, ADCB offers fast setup with no minimum balance on basic current accounts. Liv by Emirates NBD opens accounts digitally within hours once your residence visa is stamped and Emirates ID is in process, no branch visit mandatory.

- Emirates NBD — strongly favoured for corporate accounts; minimum balance AED 25,000–50,000; suits international founders seeking relationship banking

- ADCB — fast digital onboarding for corporate accounts; minimum balance AED 25,000; preferred by digital-first founders

- Mashreq — online onboarding process; minimum balance around AED 10,000 for certain corporate setups

- ADCB Personal — fast setup with no minimum balance on basic current accounts

- Liv by Emirates NBD — opens personal accounts digitally within hours once residency is stamped and Emirates ID is in process; no branch visit mandatory

Free Zone vs. Mainland: What It Means for Banking

Free Zone companies and Mainland companies follow the same banking process at the document submission stage. Free Zone setups, like those at Meydan Free Zone, offer 100% foreign ownership, digital setup, and packages tailored to consultants and tech entrepreneurs, which shortens the gap before banking can begin.

A Mainland company is the appropriate structure if you want to trade directly within the local UAE market or take on government contracts. What most South African founders discover too late: choosing Mainland when a Free Zone structure fits their business model means unnecessary cost and setup complexity, with setup running over AED 50,000 in year one.

Tax Considerations and Ongoing Administration

As of June 2023, a federal Corporate Tax of 9% applies to taxable profits above AED 375,000 annually (Federal Tax Authority, 2023). VAT at 5% is mandatory for businesses with annual revenues over AED 375,000. Free Zone companies may qualify for 0% on qualifying income from activities outside the UAE, confirm the exact threshold before you proceed.

South Africa operates a residency-based tax system. South Africans who relocate to Dubai must formally exit tax residency with SARS to avoid being taxed in both jurisdictions. A founder who draws dividends from a UAE company without completing formal tax emigration risks personal liability for South African tax on worldwide income. The UAE and South Africa have a Double Taxation Agreement, but it does not automatically resolve residency conflicts. Seeking specialist advice before you proceed is not optional.

Conclusion

Opening a corporate and personal bank account in Dubai for South Africans is sequential, not automatic. Get the Trade License issued, the Establishment Card opened and functional, the residence visa stamped, and the documentation prepared before approaching any bank. Address South African tax exit obligations with a cross-border adviser before the process starts. Done in the right order, the entire process runs from three to six weeks for most standard cases.