Table of Contents

Frequently Asked Questions

1. Does moving to Dubai automatically end my South African tax residency?

No. Physical relocation does not end South African tax residency. SARS applies an ordinarily resident test and a physical presence test, meaning founders who relocate without formally notifying SARS remain fully taxable on worldwide income. Formal tax emigration must be completed as a separate legal process.

2. What is the exit charge when leaving South Africa for the UAE?

When South African tax residency ceases, SARS triggers a deemed disposal of certain assets, including shares in private companies and investment portfolios, and capital gains tax applies to the notional gain. This exit charge is often the largest single tax cost in the entire relocation and must be budgeted for upfront before any UAE setup costs are incurred.

3. How does the South Africa-UAE Double Taxation Agreement work for entrepreneurs?

The DTA governs how income is allocated between the two jurisdictions to prevent the same income being taxed twice. However, it does not eliminate SARS's right to assess founders who have not formally ceased South African tax residency. Residency status is the threshold question, the DTA only provides protection once the formal exit is complete.

4. Do Free Zone companies in the UAE pay corporate tax?

Free Zone companies may qualify for a 0% corporate tax rate on qualifying income, but this is not automatic. Genuine substance in the Free Zone, qualifying activities, and compliance with de minimis rules on non-qualifying revenue are all mandatory. All UAE businesses must register with the Federal Tax Authority for Corporate Tax purposes regardless of whether they exceed the AED 375,000 threshold.

5. How long does the South African tax emigration process take?

The formal tax emigration process typically runs three to six months from engagement with SARS. This process must be started before or alongside the UAE setup, not as an afterthought. Founders who delay risk receiving SARS assessments covering worldwide income earned during the transition period, creating personal liability for back taxes and fines.

Topic Summary

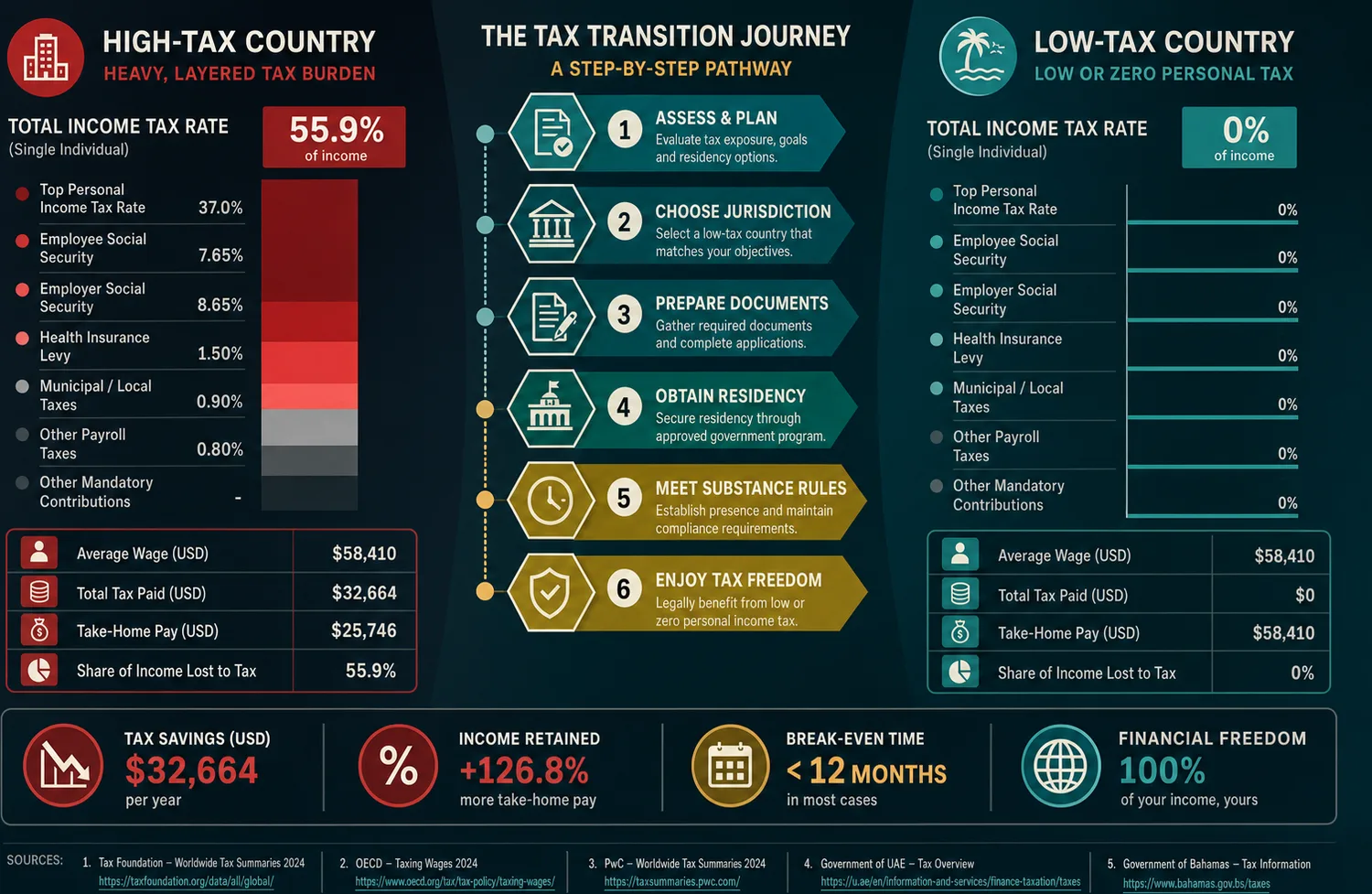

1. South Africa Tax vs UAE Tax: The Real Gap

South Africa taxes residents on worldwide income at up to 45%, while the UAE has no personal income tax. The gap is real, but only with genuine UAE residency and a clean South African exit, founders taxed in both jurisdictions simultaneously discover this too late.

2. Physical Relocation Doesn't End SARS Obligations

Moving to Dubai doesn't automatically cease South African tax residency. SARS applies an ordinarily resident test, and founders who skip formal tax emigration face personal liability for back taxes, interest, and fines covering all worldwide income earned through their UAE entity.

3. The Exit Charge Most Founders Don't Budget For

Formal tax emigration triggers a deemed disposal of assets, shares, portfolios, and private company interests all attract capital gains tax at the exit date. This is often the largest single tax cost in the entire relocation, and seeking specialist advice before the process starts is not optional.

4. UAE Corporate Tax and VAT Obligations Apply From Day One

A federal Corporate Tax of 9% applies to taxable profits above AED 375,000 annually, and VAT at 5% is mandatory once revenues exceed AED 375,000. Free Zone companies may qualify for 0% on qualifying income, but only with genuine substance, not just a registered address.

5. Free Zone vs Mainland: The Decision That Determines Cost

Most South African entrepreneurs will find a Free Zone company is the appropriate structure, 100% foreign ownership, mandatory virtual or flexi-desk office arrangements, and packages tailored to consultants and tech entrepreneurs. A Mainland company is the appropriate structure only when direct trading in the local UAE market is the core plan.

6. The South Africa-UAE DTA Doesn't Protect Unexited Founders

The Double Taxation Agreement governs how income is allocated between jurisdictions, it does not eliminate SARS's right to assess founders who have not formally ceased South African tax residency. Residency status is the threshold question, and the UAE structure delivers no tax benefit without a clean exit.

7. Realistic Budget: Four to Eight Months and Two Cost Streams

South African founders should budget ZAR 150,000–400,000 for the exit process and AED 45,000–65,000 for UAE Free Zone setup, visas, and year-one operations, plus AED 25,000–100,000 minimum bank balance. The full timeline from decision to operational entity with banking runs four to eight months.

South Africa Tax vs UAE Tax: South African Entrepreneurs Guide

South African entrepreneurs moving to Dubai aren't simply swapping one tax system for another. They're exiting one of the world's most aggressive residency-based tax regimes and entering a federal structure with no personal income tax, but with real compliance obligations most founders only discover after signing a lease in Dubai Marina. The South Africa tax vs UAE tax comparison only works in your favor when two things are true: your South African exit is formally complete, and your UAE substance is genuine.

What the Two Systems Actually Look Like Side by Side

SARS taxes South African tax residents on worldwide income at rates reaching 45% on income above ZAR 1,817,000 (SARS, 2024). Dividends carry a 20% withholding tax. Capital gains are taxed at an effective rate of up to 18% for individuals on asset disposals, including shares in private companies.

- Personal income tax rate: up to 45% on income above ZAR 1,817,000

- Dividends withholding tax: 20%

- Capital gains tax: effective rate of up to 18% for individuals

- Worldwide income taxed: all global earnings are subject to SARS assessment

- Asset disposals included: shares in private companies trigger capital gains liability

The UAE has no federal personal income tax. A 9% Corporate Tax applies to profits above AED 375,000 annually under Federal Decree-Law No. 47 of 2022, effective for financial years from 1 June 2023. VAT runs at 5%. Free Zone companies may qualify for a 0% rate on qualifying income, but only with genuine substance and active compliance, not by default.

Physical Relocation Does Not End South African Tax Residency

This is where most founders get into trouble. Moving to Dubai doesn't automatically end your South African tax obligations. SARS applies an ordinarily resident test and a physical presence test. Until you formally notify SARS, file a final return, and settle any liabilities, you remain a South African tax resident, fully assessable on worldwide income.

The exit charge is the part that catches founders off guard. A deemed disposal of certain assets is triggered at the date tax residency ceases. Founders holding shares in private companies or investment portfolios face a real capital gains tax bill before they've left. A South African founder with a private company valued at ZAR 8 million and a ZAR 3 million investment portfolio should budget approximately ZAR 280,000 for the total exit process before a single UAE cost is incurred.

The South Africa-UAE Double Taxation Agreement: What It Actually Does

The DTA between South Africa and the UAE (in force since 2016) allocates taxing rights based on where you're resident, not where income is earned. It doesn't override SARS's right to assess you if you haven't formally ceased South African tax residency. The DTA only protects you once residency has formally shifted.

Permanent establishment risk is real. A UAE-based founder who continues managing a South African company, signing contracts on its behalf, or chairing board meetings remotely creates a taxable presence in South Africa. Board meetings and key decisions should physically take place in the UAE, and that must be documented.

The UAE Setup Sequence for South African Founders

The correct order matters. Start with a cross-border adviser who understands both SARS and the UAE Federal Tax Authority before incurring any UAE costs. They'll model your exit charge, identify remaining South African income streams, and sequence the two processes correctly.

From there: choose your jurisdiction. A Free Zone company, 100% foreign ownership, no mandatory physical office, packages tailored to consultants and tech founders, is the right fit for most South African entrepreneurs. Mainland is the appropriate structure only when direct trading in the UAE local market is the core model. Once the Trade License is issued, the Immigration File opens, the Entry Permit follows, and in-country residency steps complete the sequence. The corporate bank account comes last, UAE banks need documented client contracts, projected annual revenue, and a local address before they treat the entity as commercially real.

UAE Corporate Tax and VAT: What Applies from Day One

All UAE businesses must register with the Federal Tax Authority for Corporate Tax purposes, regardless of profit level. VAT registration is mandatory once annual revenues exceed AED 375,000. Free Zone founders serving international clients may zero-rate supplies, but this requires documented proof that services were consumed outside the UAE, not an assumption.

Records must be maintained for five years minimum. Corporate Tax returns are due within nine months of the financial year end. Missing deadlines attracts fines from the Federal Tax Authority.

What the Move Actually Costs

Budget ZAR 150,000–400,000 for the South African exit process, including exit charge, adviser fees, and final filings. UAE Free Zone setup runs AED 15,000–30,000 for year one. Visa and residency costs add AED 15,000–30,000. Corporate bank minimum balances run AED 25,000–100,000. Total timeline from decision to operational UAE entity with banking: four to eight months.

The Bottom Line

South Africa tax vs UAE tax isn't a simple 45% versus 0% headline. It's a structured transition requiring a formal SARS exit, genuine UAE residency and substance, and active compliance with UAE Corporate Tax and VAT from the first financial year. The founders who execute this correctly start with a cross-border adviser, model the exit charge before committing to a move date, and follow the UAE setup sequence in order. Done properly, the structure is real and defensible. Done poorly, you're paying tax in both jurisdictions simultaneously.

Contact a cross-border adviser with South Africa-UAE experience before incurring any UAE setup costs. Address South African tax exit obligations before the process starts, not as a parallel task.