Table of Contents

Frequently Asked Questions

1. Is health insurance mandatory in Dubai for German expats?

Yes. Dubai health insurance is mandatory under Law No. 11 of 2013 for all residents, there are No exceptions. The DHA accredits providers and sets the EssentialBP as the minimum standard. Failure to maintain health insurance can result in visa renewal rejection and personal liability for treatment costs.

2. When does the Dubai health insurance obligation start?

The obligation starts the moment residency is stamped inside your passport, not from Emirates ID issuance. A German expat who waits for their physical Emirates ID card before activating coverage has been uninsured during that gap, often two to four weeks, and bears full personal liability for any treatment costs in that period.

3. Do dependents need their own separate health insurance Plan in Dubai?

Yes. Each family member on a dependent visa require a separately enrolled DHA-licensed Plan, the primary holder's policy does not extend to them. Children and spouses on your Sponsorship each need individual coverage from the date their residency is stamped, or visa renewal will be rejected.

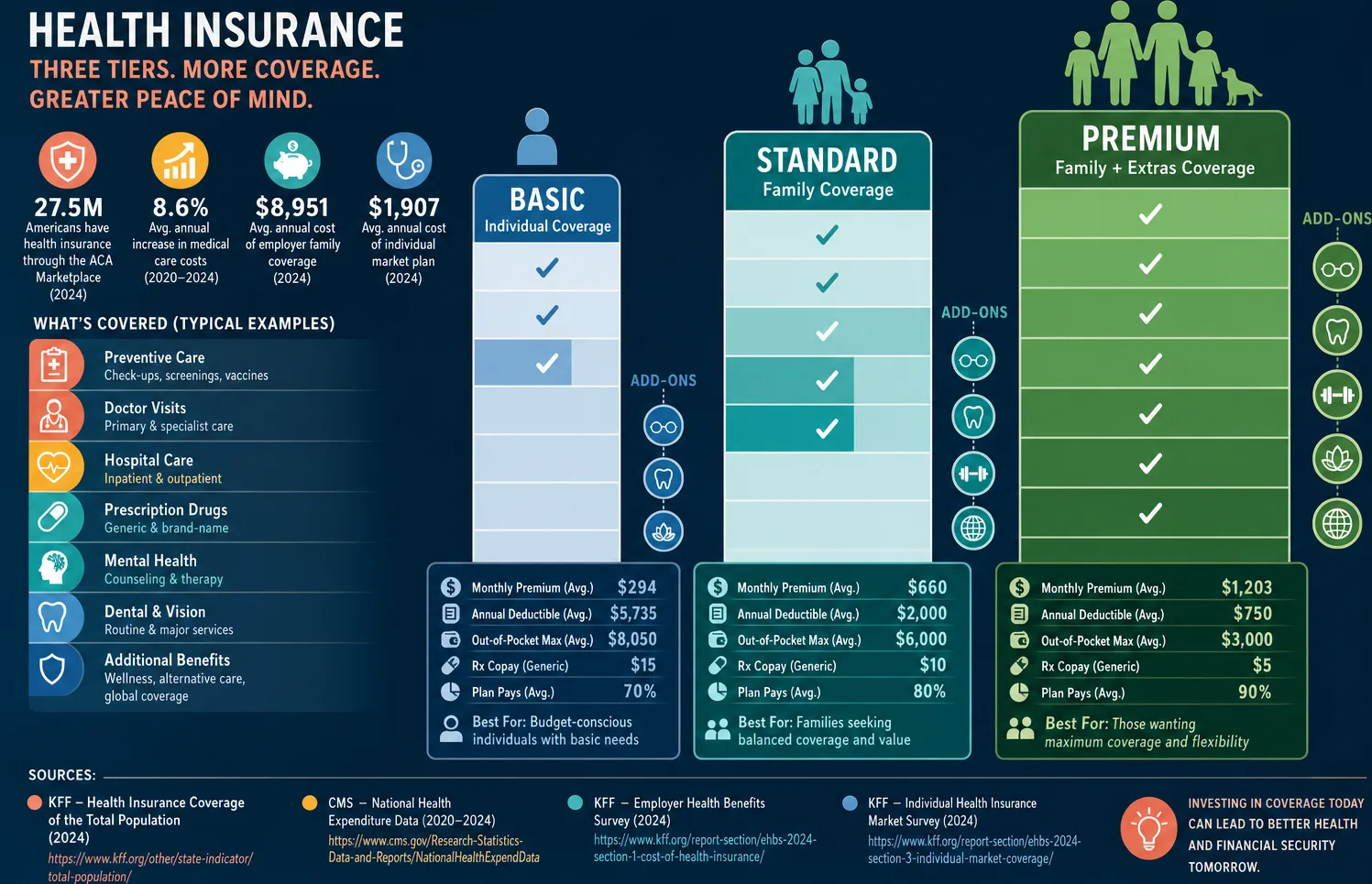

4. What does the DHA EssentialBP baseline Plan cover?

The EssentialBP covers emergency care, basic outpatient consultations, and inpatient treatment up to AED 150,000 annually for a single low-risk employee. Dental, optical, mental health, and planned maternity are often excluded from EssentialBP, these require explicit add-ons or a mid-tier Plan.

5. Does Dubai health insurance cover maternity from day one?

No. Maternity coverage carries a mandatory 12-month waiting period from policy activation. A German expat who plans pregnancy finds their insurer's waiting period means the birth is uncovered if the Plan was selected too late. An average delivery runs AED 28,000 out of pocket without the correct add-on coverage.

6. How much does health insurance cost in Dubai for a German expat family of four?

A family of four on mid-to-comprehensive coverage runs AED 25,000–50,000 annually, with plan tier and age of dependents as the primary cost drivers. Individual EssentialBP baseline plans run AED 700–1,500 annually, while comprehensive individual plans covering specialist access and chronic conditions run AED 15,000–25,000.

Topic Summary

1. Insurance Starts at Residency Stamping, Not Emirates ID

The DHA obligation triggers the moment residency is stamped inside your passport, not from Emirates ID issuance. German expats who wait for their physical card are uninsured for that gap, bearing full personal liability for any treatment costs during those weeks.

2. EssentialBP Is the Legal Floor, Not a Complete Plan

Dubai's mandatory insurance baseline covers emergency care and basic outpatient treatment up to AED 150,000 annually. Dental, optical, mental health, and maternity are often excluded, most German expats with families need mid-to-comprehensive coverage from day one.

3. Dependents Require Separate DHA-Licensed Plans

Children and spouses on the primary holder's visa require individually enrolled policies, the primary holder's coverage does not extend to them. Missing dependent enrollment creates uninsured gaps and triggers visa renewal rejection.

4. Maternity Coverage Has a Mandatory 12-Month Wait

Selecting EssentialBP or enrolling too late means the 12-month maternity waiting period leaves planned births entirely uncovered. An AED 28,000 average delivery cost falls to the insured if this is not factored in at enrollment.

5. Verify Active Status Through the DHA Portal Directly

HR confirmation alone is not sufficient confirmation that coverage is opened and functional. Log into the DHA portal before any clinic visit, a policy not yet activated will result in rejected claims even if documents were submitted.

6. Plan Tier and Network Choice Determine Real Coverage

Confirm the network includes their preferred provider before signing any plan. German-speaking clinics are not standard across all networks and must be verified separately, two distinct checks that most expats discover too late.

7. Tax Considerations Require a Cross-Border Adviser

Dubai has no personal income tax, so premiums are a full out-of-pocket cost with no offset. German expats retaining any German tax residency should seek specialist advice from a cross-border adviser before the process starts, not as a parallel task.

Healthcare and Medical Insurance in Dubai for German Expats

Healthcare in Dubai for German expats is mandatory under Dubai Law No. 11 of 2013, not an optional benefit. The Dubai Health Authority (DHA) mandates active, DHA-licensed health insurance for all residents from the date residency is stamped, not from Emirates ID issuance. Time to get covered: 3–7 business days once residency is stamped.

A Munich founder who receives their Entry Permit by email and enters Dubai should have insurance active before attending any medical appointment, not after Emirates ID delivery.

What the DHA Mandate Actually Requires

Dubai health insurance is mandatory under Law No. 11 of 2013. The DHA accredits providers and sets the EssentialBP baseline Plan as the minimum standard. No exceptions, the obligation starts the moment residency is stamped inside your passport.

If the employer is the Sponsorship holder, they bear the insurance obligation. Self-sponsored founders bear it themselves. Dependent visas require a separate family plan, they do not extend automatically from the primary holder's policy. A German management consultant on a Free Zone self-sponsorship visa must select their own coverage; the Free Zone does not provide it.

Plan Tier Comparison: Each Level Covers

Dental and optical are often excluded from EssentialBP and require explicit add-ons. Missing maternity waiting periods and chronic conditions are the two most common gaps German expats discover too late. An expat couple relocating from Frankfurt who selects EssentialBP for cost control and then plans a family will face an AED 28,000 average delivery cost entirely out of pocket.

A Numbered Process: How to Get Covered

Getting DHA-compliant health insurance follows a defined process: confirm visa Sponsorship and coverage obligation, define coverage scope, select a Licensed Plan, Submit of the following Documents, collect Your Insurance Card, and Verify Active Status on the DHA portal before the first clinic visit.

- Confirm Sponsorship: Determine whether the employer, Free Zone, or you personally bear the insurance obligation.

- Emergency coverage scope: List each family member on the visa, their ages, any chronic conditions, and planned maternity.

- Select a Licensed Plan: Choose from DHA-approved insurers only, check the DHA portal for the current approved list.

- Submit of the following Documents: Passport copy, optical Emirates ID in process or being compiled, visa copy, and a high-quality photograph with a white background.

- Maternity: Specify dental and optical add-ons at plan selection, adding them post-enrollment often triggers new waiting periods.

- Collect Your Insurance Card: Allow three to five business days, the card is not same-day.

- Verify Active Status: Log into the DHA portal before the first clinic visit, HR confirmation alone is not sufficient confirmation.

Most Expats Discover Too Late: Compliance Consequences

The insurance obligation starts the moment residency is stamped, not from Emirates ID issuance. A founder whose residency was stamped on 1 March but who activated insurance on 20 March when the Emirates ID arrived was personally liable for any treatment costs during those 19 days, there is no grace period under DHA Law No. 11 of 2013.

Each family member on your visa have their own separately enrolled DHA-licensed Plan. The sponsor is the Coverage Responsibility holder, if a dependent's policy lapses, the sponsor faces renewal rejection. Set calendar reminders 90, 60, and 30 days before each renewal date. Notify the insurer immediately of any change in visa status that requires a policy update, sponsor changes, visa category changes, and any dependent additions must be reported.

Seeking specialist advice from a cross-border adviser before you proceed is not optional if German tax exit obligations and Dubai insurance costs run simultaneously. Keep reliable wage records and insurance renewal confirmations for each family member, the DHA portal is the authoritative record, not insurer confirmation alone.