Table of Contents

Frequently Asked Questions

1. What are the main tax differences between the UK and UAE for entrepreneurs?

The biggest contrast is personal tax; the UAE has 0% personal income tax, while the UK's rates reach up to 45%. For businesses, the UAE has a 9% corporate tax on profits over AED 375,000, which is lower than the UK's main rate. Many businesses in UAE free zones can also qualify for a 0% corporate tax rate.

2. Do I automatically stop paying UK tax if I move to Dubai?

No, moving does not automatically end your UK tax obligations. You must formally cease to be a UK tax resident by meeting the criteria of the Statutory Residence Test. Any income still sourced from the UK, such as from rental properties, may remain taxable by HMRC even after you move.

3. What are the main tax benefits of moving to Dubai for UK entrepreneurs?

The primary benefit is the 0% tax on personal income, including salaries and dividends, allowing you to retain more wealth. Additionally, entrepreneurs can leverage 0% corporate tax rates in many free zones and the absence of capital gains tax. This creates a highly efficient environment for business growth.

4. How does my business setup in Dubai affect my taxes?

Your business structure is crucial for tax planning. Setting up in a designated free zone may qualify your business for a 0% corporate tax rate, while a mainland company will be subject to the standard 9% rate on applicable profits. Your choice impacts tax liability, ownership rules, and market access.

5. What are common tax mistakes to avoid when moving from the UK to Dubai?

A common mistake is failing to properly break UK tax residency, which can leave your worldwide income taxable in the UK. Another trap is keeping the 'management and control' of your business in the UK, which can make it UK tax resident. Always maintain clear records and ensure strategic decisions are made in the UAE.

Topic Summary

1. First, Pinpoint Your UK Tax Residency Status

Before anything else, you must determine if you will successfully break UK tax residency. Your status dictates your ongoing liability for UK income tax and capital gains tax, making it the single most critical step in your relocation plan.

2. Look Beyond 0% Personal Income Tax

The absence of personal income tax is a major draw, but it isn't the whole story. British entrepreneurs must also factor in the UAE's 9% corporate tax and 5% VAT to accurately calculate the real tax benefits of moving to Dubai.

3. Choose the Right Dubai Business Structure

Your choice between a mainland or free zone company has significant tax and operational consequences. This decision directly impacts your corporate tax liabilities, ownership rules, and visa eligibility, so align it with your business model from the start.

4. Manage Your Ongoing UK Connections

Physically leaving the UK doesn't automatically sever all tax ties. Income from UK property or certain business activities may still be taxable there, so it's vital to identify and plan for any UK-sourced income to avoid surprises.

5. Avoid Costly Management and Control Traps

Be careful where key business decisions are made. A UK company managed from Dubai could shift its tax residency, while managing your new UAE firm from the UK could inadvertently create a UK tax presence for it.

6. Keep Meticulous Records from Day One

HMRC requires clear proof that you have genuinely relocated. Maintain detailed travel logs, flight records, and evidence of your new life in Dubai to robustly defend your non-resident tax status if it is ever challenged.

UK Tax vs UAE Tax: Guide for British Entrepreneurs

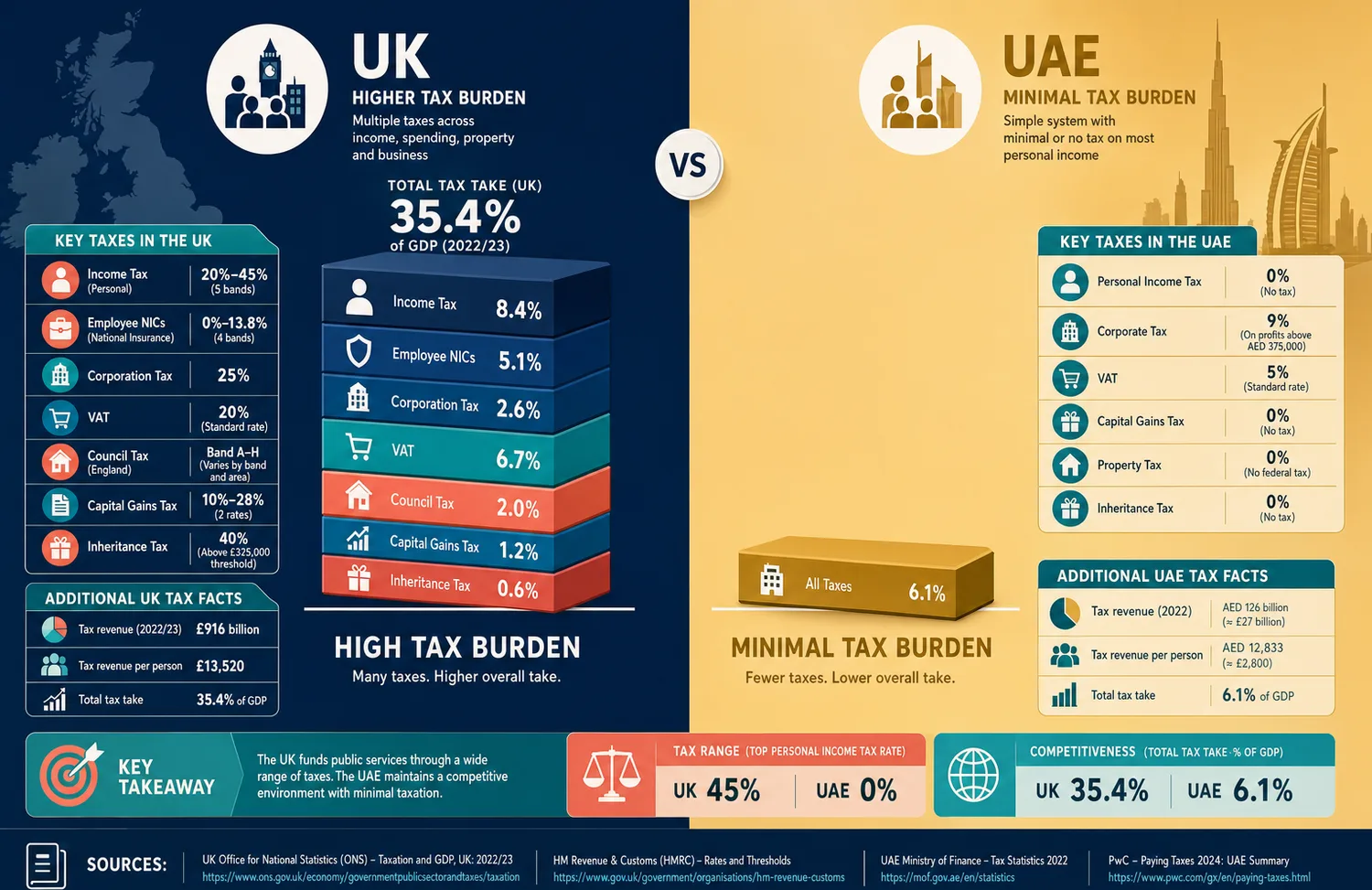

UK tax vs UAE tax comes down to one fundamental contrast: the UK taxes you on income, capital gains, and company profits through a broad, interconnected system, while the UAE presents a dramatically different picture at the federal level.

The UK applies Income Tax at 20–45%, a flat 25% Corporation Tax, Capital Gains Tax reaching 28% on some assets, and National Insurance contributions on top. The UAE, by contrast, levies no personal income tax and dividends drawn from your UAE company are yours to keep at the federal level.

However, the comparison isn't simply "pay nothing." As of June 2023, a federal Corporate Tax of 9% applies to taxable profits above AED 375,000 annually; startups below this threshold are taxed at 0%. UAE tax for British citizens only becomes fully effective once genuine residency and substance are established, a point many founders miss entirely.

UAE Tax Rules and VAT Registration Thresholds

Businesses operating in the UAE must comply with specific tax obligations depending on their revenue levels and activity. Any business with annual taxable supplies exceeding AED 375,000 is required to register for VAT at 5% with the Federal Tax Authority. This registration is not optional and must be completed once the threshold is met, not treated as a later-stage consideration.

It is also important to note that the UAE does not impose inheritance tax, which is a key structural advantage for individuals and businesses operating within the jurisdiction. Understanding these thresholds and ensuring VAT compliance from the outset helps avoid penalties and ensures your business is correctly structured from day one.

Tax Residency, Management and Source of Income Rules

A company’s tax position is not determined solely by where it is incorporated, but by where it is actually managed and controlled. If strategic decisions for a UK company continue to be made in the UK, the business may still be considered UK tax resident, potentially resulting in exposure to tax obligations in both jurisdictions.

To avoid this risk, management and control should clearly shift to the UAE once relocation occurs. This includes holding board meetings physically in the UAE and ensuring that key strategic decisions are made through a UAE-based governance structure, rather than being directed from abroad.

At the same time, it is important to understand that UK-sourced income can remain taxable in the UK even after relocation. This includes passive rental income, dividends from UK companies, or returns from UK property holdings. Because tax residency and income source rules operate independently, obtaining tailored advice on where control is exercised and how income is classified is essential before structuring or relocating your business.

Prerequisites Before You Compare UK Tax vs UAE Tax

Gather the Tools and Records

Before comparing UK tax vs UAE tax properly, you need the right records in front of you. These typically include:

- Last two years of personal Self Assessment records

- Travel history showing days spent in the UK

- Details of any UK-source income streams (passive rental income, dividends, interest)

- Current corporate structure and ownership structure documents

- UK company shareholdings and any visa-related paperwork

Gather these before you contact any adviser or begin modelling numbers. Having the right records in front of you turns a general idea into one that is clear, defensible, and ready for execution.

Confirm the Knowledge You Need

You need to be able to answer these questions with confidence before you proceed:

- What is your projected annual revenue from UK-source income?

- Do you understand how the SRT determines your tax resident status based on days spent in the UK?

- Do you understand your company's ownership structure and where key decisions are made?

Set a Time Budget and Internal Deadline

Set a clear internal deadline, ideally 60 to 90 days before your planned departure. Address UK tax exit obligations before the process starts; this is not optional. Model the before-and-after numbers on a single page so you can summarise it clearly. A relocation Plan built on real numbers before you proceed to company setup is far stronger than one assembled under pressure.

1. Review Your Current Tax Position Before You Leave

Map Your Personal Income Streams

The first and most critical step in a relocation Plan is mapping every income stream before departure. Common examples of income that remains subject to UK tax after departure include:

- Passive rental income from a UK property portfolio

- Dividends from a UK company where you hold shares

- Interest from UK bank accounts

- Employment or director income from a UK employer

Dubai tax for UK expats doesn't eliminate these obligations. You'll still need to file a Self Assessment tax return each year covering these. Factor in recurring fees for ongoing UK compliance even after you move.

Test Your Tax Residency Status

HMRC uses the SRT to determine when you cease to be a UK tax resident. The SRT looks at automatic overseas tests, automatic UK tests, and sufficient ties tests, generally, spending fewer than 46 days in the UK each year and cutting sufficient ties to the country. UAE tax for British citizens isn't simply "pay nothing", it's a position that requires you to pass these tests cleanly.

Statutory Residence Test guidance confirms that residency status based on days spent in the UK and your physical location throughout the year determines your exposure. If you fail the automatic overseas tests, you could remain a UK tax resident even while living in Dubai.

Model the Before-and-After Numbers

Summarise it on a single page. Your model should show:

- Current UK tax bill: Income Tax, Corporation Tax, National Insurance

- Projected UAE tax bill: Corporate Tax (if applicable) and VAT (if registered)

- UK tax obligations on source income remaining after departure

- Net actual saving after UAE setup, residency, and annual renewal prices are factored in

Model the actual saving based on real numbers before you proceed to company setup. This single page becomes your decision document.

2. Choose the Right UAE Company Setup and Visa Sequence

Match the Structure to the Scope of Business

The tax benefits of moving to Dubai depend heavily on choosing the right structure. A Free Zone company is often a perfect fit as it allows 100% foreign ownership, packages tailored to consultants and tech entrepreneurs, and mandatory virtual or flexi-desk office arrangements that keep setup prices manageable. It's the right fit when you don't need to trade directly within the local UAE market or require unrestricted commercial access.

A Mainland company is the appropriate structure if you want to trade directly within the local UAE market, take on government contracts, or operate from any location. It's regulated by the Department of Economic Development and comes with higher setup prices and mandatory physical office space, which can cost over AED 50,000 annually.

Follow the Company Setup and Visa Process

Follow this sequence precisely:

- Choose jurisdiction: Free Zone (ease of setup, 100% ownership) or Mainland

- Select a specific activity from a government-approved list, don't just pick a generic "consulting" label

- Submit documents, Trade License

- Open the Immigration File (Establishment Card), without it, no visa process starts

- Apply for the Entry Permit, allowing the founder to enter the UAE

- Complete residency steps: medical fitness test, Emirates ID process, and visa stamping

Know What You Should See After This Step

After this step, you should hold a valid Trade License, an open Immigration File, and a residence visa stamped inside your passport, typically valid for two years. Your visa allocation needs and license activity are both confirmed. This gives you a functional corporate base from which the rest of the Plan proceeds.

3. Move: Physically Relocate to the UAE and Shift Management to the UAE

Complete the Physical Relocation Properly

Relocating is not only about getting a visa. UAE tax for British citizens only becomes a legally distinct tax position, but only once the physical move is genuine and documented. You must spend enough time in the UAE to satisfy the SRT's automatic overseas tests, generally fewer than 46 days in the UK in the tax year following your departure.

Keep hotel receipts that confirm your physical location throughout the year. Save boarding passes, utility bills, and tenancy agreements. If HMRC ever questions your non-resident status, this evidence is crucial to prove it.

Shift Board and Management Activity

Once you move, your board meetings physically take place in the UAE. Strategic decisions are made by a UAE-based process. If your company is genuinely managed from Dubai, HMRC cannot claim it remains UK tax resident under the central management and control test.

To mitigate this risk, ensure that once you move, you keep minutes of all board meetings held in the UAE, and you keep minutes confirming where key decisions are made. This Management Activity record is non-negotiable.

Document the Evidence Trail

A documented trail protects your position. Keep records of:

- Days spent in each country, with passport stamps as supporting evidence

- Board meeting minutes held in the UAE

- Signed contracts and invoices issued from your UAE company

- Bank statements confirming UAE-based transactions

4. Handle Ongoing Taxes, VAT, and UK Source Income

Manage UAE Corporate Tax and VAT

Dubai tax for UK expats doesn't end at setup. As of June 2023, a federal Corporate Tax of 9% applies to taxable profits above AED 375,000. Free Zone companies can access a 0% rate for qualifying income, but only with genuine substance, not just a registered address. Businesses with annual revenues over AED 375,000 must register for VAT at 5% with the Federal Tax Authority.

Know What Success Looks Like Here

Your business is compliant when Corporate Tax and VAT registration is completed with the Federal Tax Authority, UK source income is declared via Self Assessment, and your record trail supports your non-resident position. Keep reliable wage records, maintain health insurance as a required condition of UAE residency, and run both compliance calendars simultaneously.

Success Criteria and Next Steps for UK Tax vs UAE Tax

Check Your Success Criteria

You've completed this process successfully when all of the following are in place:

- Company legally formed with Trade License and Immigration File opened and functional

- Residence visa stamped inside your passport, typically valid for two years

- SRT from a clear departure date confirmed with a cross-border adviser

- Corporate bank account opened and your record trail supports your non-resident position

- UK source income obligations identified and annual filings planned

UK tax vs UAE tax is no longer a general question at this stage, it becomes a documented Plan with clear filings, ownership decisions, and operating procedures.

Conclusion

To build momentum this week: define your business activity, choose jurisdiction (Free Zone or Mainland) in week one, and model the saving based on real numbers before you proceed. Contact a specialist who can provide a detailed UK-UAE tax comparison covering your specific income streams, corporate structure, and planned departure date. Having these ready saves time and prevents the most common errors British entrepreneurs considering relocation discover too late.